Adapting to a challenging market: Three Nordic companies share their financing strategies

A decade of cheap and ample Nordic corporate bond financing came to an abrupt end in 2022 amid soaring inflation and rising interest rates. How are companies adapting to the new normal? Three Nordic corporates shared their approach to funding with Nordea's Henrik Immelborn at the recent Treasury 360 Nordic conference.

The market environment for funding has changed dramatically in the past 18-24 months. 2022 marked a clear shift both in the availability of capital and the pricing of risk, compared to previous years since the financial crisis. It now costs more money to borrow money whether you’re a government, an investment grade or high-yield corporate or a household.

With high inflation and rising interest rates, paired with risk aversion, how are corporate treasuries responding to the new world order?

That was the focus of Nordea’s panel at the recent Treasury 360° Nordic event in Malmö in April, which brought together 500 treasury and finance professionals from across the Nordics. The panel, “Navigating a storm,” featured three Nordic companies that have responded in different ways to the changing market environment.

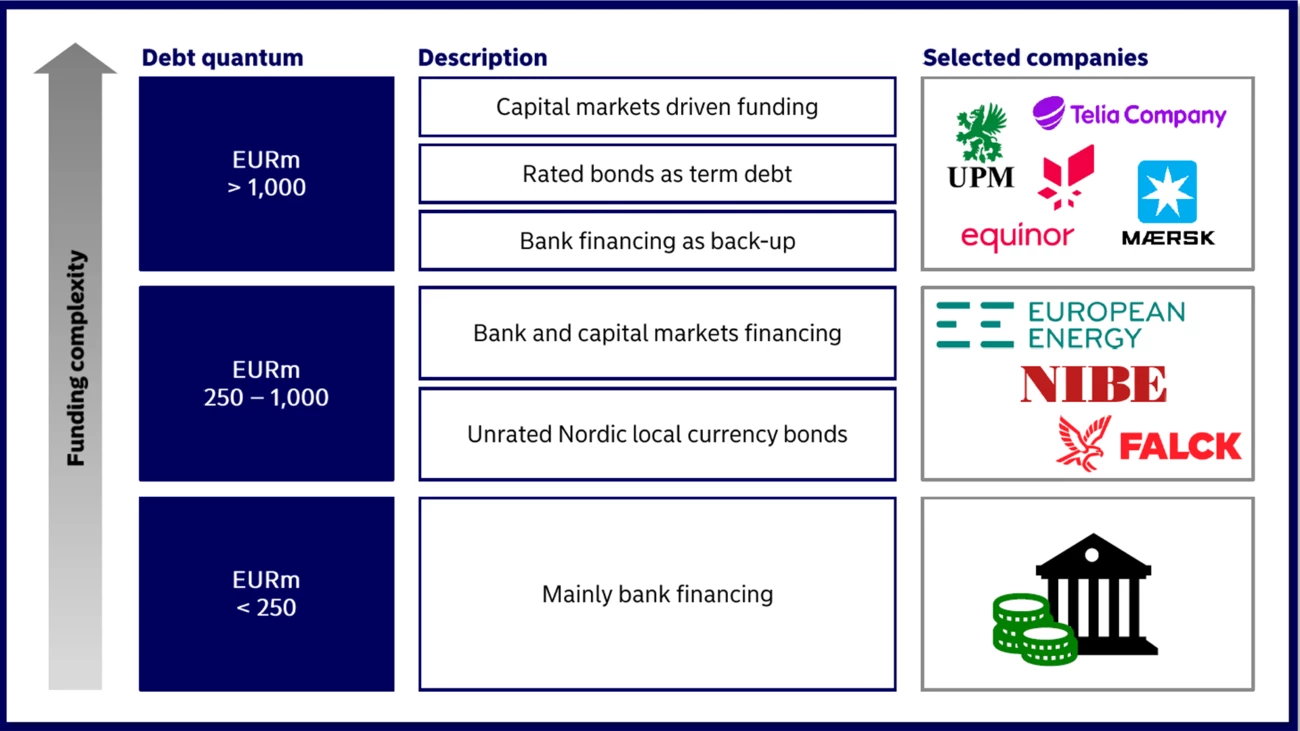

More debt, more funding complexity

Nordea’s Henrik Immelborn, Managing Director, Debt Solutions and Loans, kicked off the discussion by presenting a framework illustrating how companies’ funding complexity and diversification typically increases with their absolute amount of debt. On the top tier, with debt over EUR 1,000 million are the large blue-chip corporates, with rated bonds as term debt and bank financing as a back-up. On the middle tier, with debt between EUR 250-1,000 million, are companies that rely on a mix of bank and capital markets funding, primarily in the form of unrated Nordic local currency bonds. And on the bottom, with less than EUR 250 million in debt, are companies that rely primarily on bank financing.

In many ways, the most interesting segment is the middle segment, with debt between EUR 250-1,000 million, as they are the most impacted by the shift in market conditions.

“In many ways, the most interesting segment is the middle segment, with debt between EUR 250-1,000 million, as they are the most impacted by the shift in market conditions,” said Immelborn, noting that the unrated Nordic bond markets are not available to the same extent as in the past.

“Do these companies accelerate their journey to a credit rating to move up to the most advanced layer? Or do they go in the other direction and become more dependent on bank financing?” he asked.

The three companies represented on the panel, Falck, NIBE Group and European Energy, are all in the middle segment, and each has taken a different approach in the new funding environment.

Source: Nordea

Allan Kristoffersen, Head of Global Treasury, Falck

Sticking to bank financing

Falck, the Denmark-based healthcare and emergency company, is privately owned with a few long-term institutional investors with significant financial resources. Head of Global Treasury Allan Kristoffersen explained that the company in the first quarter of 2022 undertook a deep-dive review of its funding diversification. While the company concluded that it could go to the bond market, it decided not to and rather stick to its strategy of relying on bank financing from its five core relationship banks.

“We were concerned about the potential lack of flexibility in having multiple layers of funding in different scenarios,” Kristoffersen said.

He noted that with a bond issue, “you have a specific point in time you need to manage very carefully.” A longstanding bank relationship allows for closer dialogue and flexibility in times of change, he added.

While Falck is not considering getting a public credit rating, it is focusing on ESG when it comes to funding.

“Having an ESG link to our funding has enormously propelled the whole ESG agenda,” he said. Falck signed a sustainability-linked credit facility in 2021. “The increased focus on the ‘S’ in ESG lines up with Falck’s mission, and we’re investigating how we can make further use of that,” he added.

Tina Nguyen, Finance and Treasury, NIBE

Bond market challenges

The largest company on the panel, NIBE Group, has previously been an active issuer in the local bond market, but has post pandemic decided not to issue any bonds due to unfavourable market conditions. The Swedish producer of heat pumps and climate solutions has a strong credit profile, low leverage and a sizeable cash flow. A large part of the company’s liquidity reserves is cash flows from its operations, explained Tina Nguyen from Finance and Treasury at NIBE.

In 2015, NIBE entered the bond market, issuing bonds totalling SEK 1.5 billion under its newly established MTN (medium-term note) program. The company has issued several bonds since, with different maturities. It also has a multicurrency RCF (revolving credit facility) and term loans with a few selected house banks.

“The RCF allows us to be quite flexible. Within a few days, we can utilise loans within a certain amount and certain currency,” she said. NIBE has an intensive acquisition strategy, and for a large acquisition, the company can pay with shares, she added.

Nguyen noted that NIBE has not issued bonds for some time due to the current uncertainty and volatility of the local bond market. She said the company is looking at acquiring a public credit rating as the next step to “open the doors for more options.” With only nine people working at NIBE’s headquarters, the time and resources needed to obtain a credit rating have been limiting factors.

“Behind all the numbers, there are people. A public rating is something we will be facing. When remains to be seen. Probably when we are 12 people,” she said with a smile.

Flemming Jacobsen, Head of Group Treasury and FP&A, European Energy

Eyeing a public credit rating

Another company looking at a credit rating is European Energy, the Danish developer of wind and solar parks. The privately-owned company has been on a rapid growth trajectory, growing 60% in 2022, which comes with an increasing funding need, currently around EUR 900 million annually. The company is leveraged with bonds in the Nordic unrated high-yield market and also relies on project financing from investors and banks.

While project financing has remained strong in the current market environment, the bond market has been more problematic, said Flemming Jacobsen, Head of Group Treasury and FP&A at European Energy.

“It can take up to a month to prepare for a new bond issue. At that point, the market can be closed down. A rating is relevant in times of volatility and uncertainty. It’s something we’re thinking about,” he said.

Until now, European Energy has been too small to justify a public credit rating. However, with close to EUR 135 million of EBITDA for 2022, the company is approaching the needed size, according to Jacobsen. The main challenge is the lack of rated peers and no given methodology for the rating agencies to apply.

“It’s not as straightforward as one would think. But we would like to continue to use the Nordic high-yield bond market, preferably with a rating,” he said.

Nordea’s Immelborn noted that the Basel IV banking reforms could also affect banks’ lending to corporates, making a public credit rating even more relevant in the near future.

It can take up to a month to prepare for a new bond issue. At that point, the market can be closed down.

Going forward

It is evident that the current market environment presents both opportunities and challenges for corporate treasurers. Immelborn summarises: “We live in interesting times. Our work as advisors to our corporate clients around financing has never been more complex and dynamic. At the same time, it’s a real opportunity to have a strategic dialogue and actually make a difference. That’s what makes our job as bankers so interesting.”

Nordic companies stick to climate goals despite global uncertainty

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

RESourceEU in the age of geoeconomics: Nordic companies positioned to seize opportunities

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

How APIs power the real-time payments revolution in banking

The financial industry is right now in the middle of a paradigm shift as real-time payments become the norm rather than the exception. At the heart of this transformation are banking APIs (application programming interfaces) that enable instant, secure and programmable money movement.