The current status of Open Banking – and a glimpse into the future

In this special guest blog for Nordea, Mounaim Cortet shares the key findings from INNOPAY’s most recent Open Banking Monitor, with a special focus on Nordea as well as the future of Open Finance.

Existing players step up their game and new players enter the arena

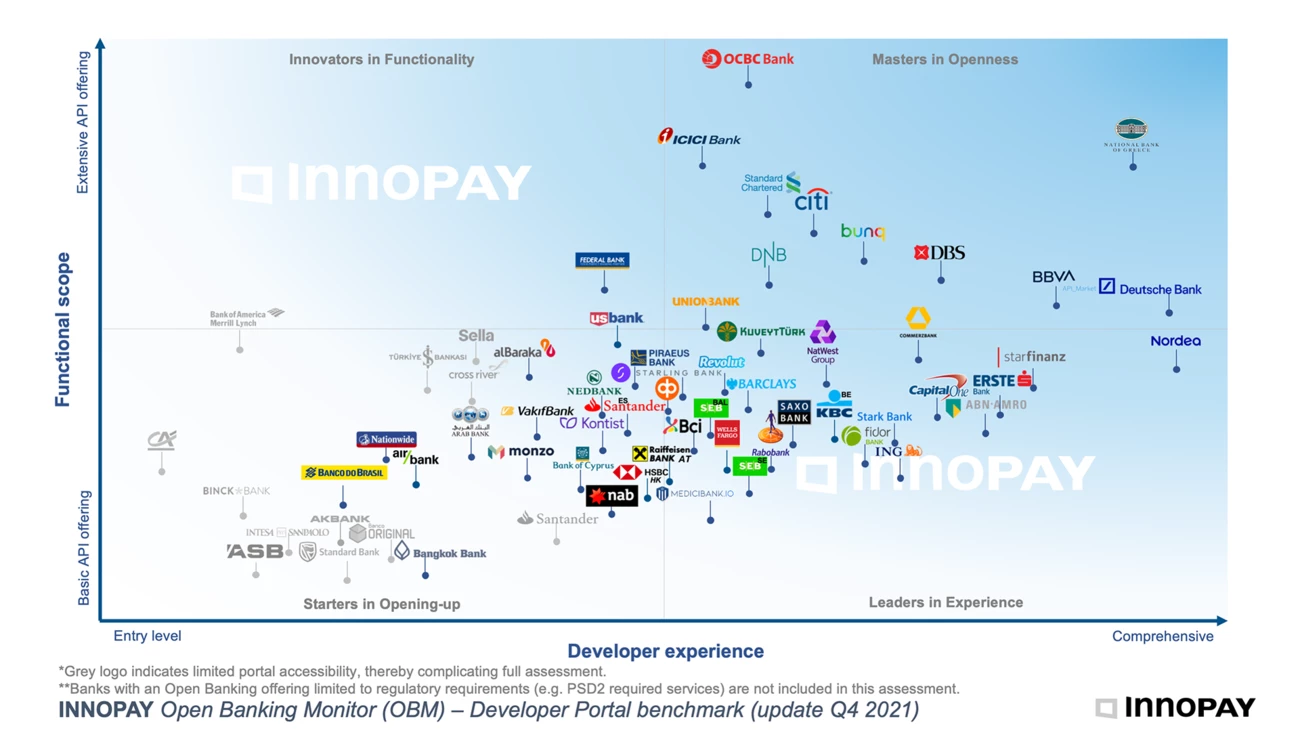

INNOPAY’s Open Banking Monitor shows the efforts banks are making in expanding their API product offering (the ‘Functional scope’ axis) and in improving the experience for API consumers (the ‘Developer experience’ axis). The latest edition of the Open Banking Monitor shows that existing players are stepping up their game and providing interesting Open Banking product propositions. Meanwhile, new banks are entering the arena.

Growing API product offering

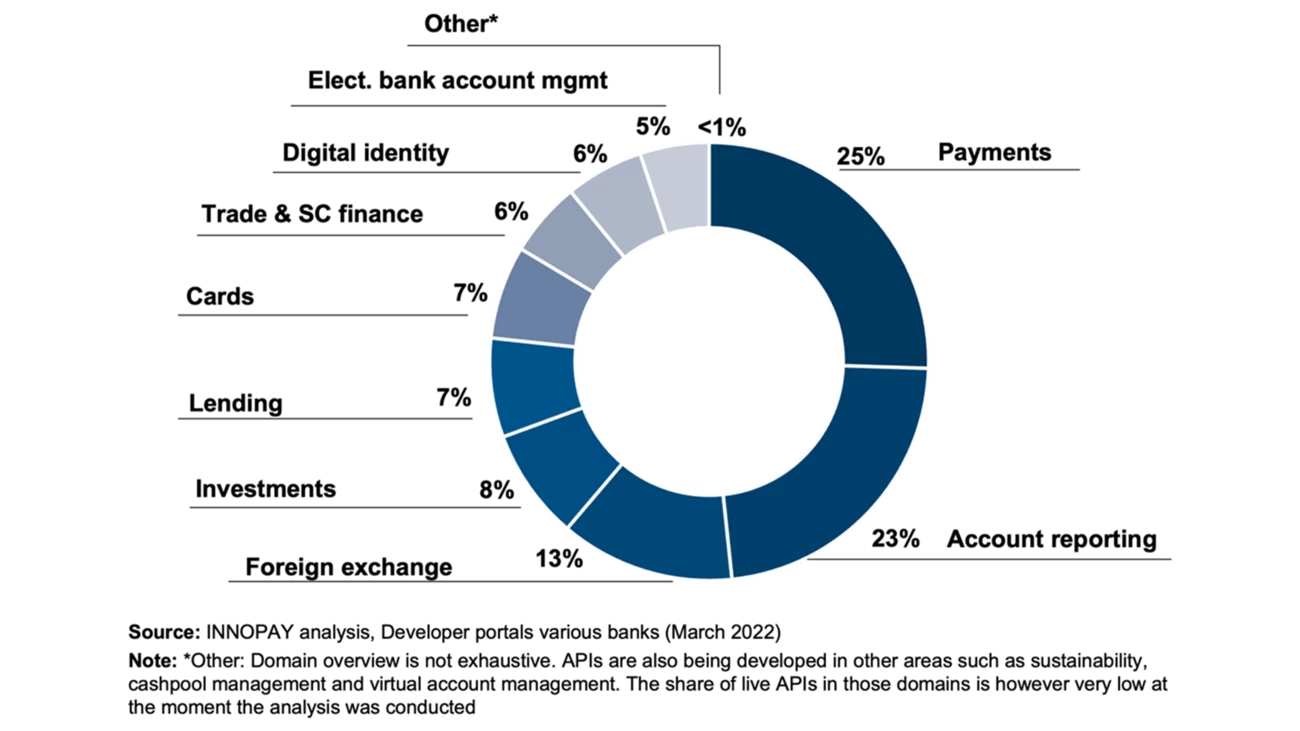

Notably, there is a trend towards banks offering more APIs, indicated by a 17% increase in APIs offered per bank. The APIs now cover a broader variety of common banking functionalities, but account information (for various account types), payment initiation (for various payment instruments) and payment management (for various user-initiated actions around the payment) still top the list. These are followed by customer information APIs (enabling the controlled sharing of selected data attributes), which have increased considerably. Similarly, a variety of corporate APIs have hit the market, further driving efficiencies and improved customer experience in transaction banking operations (e.g. trade finance, electronic bank account management (eBAM) and real-time cash pooling capabilities).

"Notably, there is a 17 % increase in APIs offered per bank."

While Open Banking APIs still focus on core functionality, adoption is accelerating and spreading to other products and services, as shown in the image visualising our analysis of APIs in the developer portals of 15 large multinational banks.

APIs per domain based on INNOPAY’s analysis of the developer portals of 15 large multinational banks.

Improved developer experience

The average developer experience score has increased by 11%. This raises the bar, meaning that competition is intensifying and banks need to step up their game to avoid falling behind their peers. The improvement in developer experience is mainly driven by:

Community Development: 22% increase in banks actively investing in community development efforts through news articles, blogs, events or partnership programmes. This indicates that banks are picking up on the importance of establishing an Open Banking community to drive innovation.

Developer Usability: 21% increase thanks to additional – or optimised – development tools such as dynamic sandbox functionalities, detailed ‘getting started’ guides or more comprehensive application and credential management features, contributing to a better developer experience by making life easier for API consumers.

API Documentation: 3% increase in features such as information on API business context, API versioning & changelogs and conciseness of the API specifications, all of which improve the overall readability of the API documentation and related content.

“Open Banking is not all about exposing and consuming data and functionalities, even more so it is about exploring new possibilities enabled through open business models”.

Three Open Banking trends to enhance the developer experience

We currently observe three trends that play an important role in enhancing the experience of API consumers:

Consistent developer experience across countries and markets

API solutions solve a wide array of challenges for a variety of API consumers across multiple verticals and markets. A key differentiator for banks is being able to retain a consistent and intuitive experience, to ensure interoperability of their solutions, through a unified approach.

Collaborative solutions through “Partner APIs” or “Mash-ups”

Open Banking is not all about exposing and consuming data and functionalities, even more so it is about exploring new possibilities enabled through open business models. Banks with a collaborative mindset can establish a key position within new digital ecosystems by co-creating new mutually beneficial products in complete user journeys.

Flexible API solutions catering for diverging needs

There is no one-size-fits-all solution, and the needs of specific API consumers might differ in terms of security and authentication requirements or API formatting preferences. With this in mind, API solutions that cater for flexibility, increase overall robustness and stimulate adoption at scale.

Open Banking and Nordea – the frontrunner in developer experience

Nordea was one of the first banks in Europe to take a proactive approach to Open Banking back in 2017 and is therefore a familiar face in the Open Banking Monitor. When it comes to the developer experience, Nordea has ranked among the top players ever since the start of our ranking, and this year it took the leap to become the frontrunner in this area.

So what is it about Nordea that makes it so successful in this respect? Well, to start with, Nordea is the top-performing bank regarding developer usability. Developers are supported by a wide array of information, tutorials and ‘how-to’ guides. App management features include organisation and certificate management capabilities. Sandbox functionalities include dynamic data and test-user management.

“When it comes to the developer experience, Nordea has ranked among the top players ever since the start of our ranking, and this year it took the leap to become the frontrunner in this area.”

Secondly, community development and engagement activities are well represented at Nordea, with active participation in the Open Banking market, for example through internal and external events, participation in different forums, blogs, customer cases, newsletters and social media interactions. In addition, community-developed tools and projects are frequently highlighted and promoted, stimulating others to participate. Nordea is deeply involved in community management activities, for example by inviting API consumers to help develop new APIs and by collecting feedback from third parties to drive API management improvements. Right from the start of its Open Banking journey, Nordea has continuously used the knowledge gained from the PSD2 API scope to benefit the creation of its commercial APIs.

Thirdly, when it comes to API documentation, Nordea makes a clear distinction between business and technical documentation to take different types of visitors on their developer portal into account. Nordea’s developer portal has recently undergone a transformation into ‘Nordea API Market’. It still caters for all the required technical elements considered in the OBM Capability model, but now also fulfils the needs of business users by presenting API use cases and offerings, a library of recent newsletters and a display of awards and rankings.

Three functional aspects of Open Banking to consider

When it comes to the functional scope of the Open Banking Monitor, three aspects are considered when comparing API functionalities:

Comprehensiveness of the API product

The value enabled through the API

The complexity of the API.

Nordea’s FX Trading API product is a good example of where these aspects come together. It covers a multitude of APIs across the complete trade chain (i.e. from access to real-time FX rates, to executing FX spots and swaps and retrieving post-trade reports).

It’s time to act – Open Finance is just around the corner

For everyone in the Open Banking space, regardless of whether they are frontrunners like Nordea or taking a more reactive approach, there is now a new challenge on the horizon: ‘Open Finance.’ In this emerging paradigm in the financial services industry, value creation will come from sharing, providing and leveraging access to even more banking data and products through APIs. Open Finance is designed to support the development of more compelling, 'embedded' value propositions and experiences for customers and partners in digital ecosystems.

“Open Finance is a game changer that challenges financial institutions to rethink their business models and get involved in order to unlock business value and secure their relevance.”

Besides the compliance challenges of Open Finance, financial services providers and other actors need to cope with an ever-changing competitive landscape. Emerging players are disrupting traditional value propositions and business models while simultaneously also presenting new opportunities for collaboration. We see a broad shift towards value creation happening in ecosystems, facilitated by seamless digital customer journeys and data flows. Organisations that execute ambitious Open Finance strategies are likely to come out on top in this data-driven economy.

Open Finance is a game changer that challenges financial institutions to rethink their business models and get involved to unlock business value and secure their relevance. It is safe to say that Open Finance is the key building block for financial service providers who wish to compete and collaborate in digital ecosystems. It is time for them to act.

About Mounaim Cortet

Mounaim Cortet is Director and Country Lead at INNOPAY for the DACH region. He is a seasoned strategist who is fascinated by the nexus of business strategy and the growing opportunities of regulation, data and technology. He works on strategic and innovation-related challenges in Payments, Digital Identity and Open Finance and – more broadly – the digital transactions space.

About INNOPAY

At INNOPAY, a consultancy firm specialised in digital transactions, our mission is to guide organisations worldwide to fully embrace the opportunities of the digital transactions era. We monitor the developments of the Open Banking landscape with great interest and we share our insights and analysis with the community through our Open Banking Monitor.

Nordic companies stick to climate goals despite global uncertainty

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

RESourceEU in the age of geoeconomics: Nordic companies positioned to seize opportunities

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

How APIs power the real-time payments revolution in banking

The financial industry is right now in the middle of a paradigm shift as real-time payments become the norm rather than the exception. At the heart of this transformation are banking APIs (application programming interfaces) that enable instant, secure and programmable money movement.