Insights

A strong ESG score requires both actual improvement and communication of it

Sustainability has become the norm in financial markets, driving a massive demand for ESG data and services. Nordea's Head of Sustainable Finance Advisory Jacob Michaelsen reflects on how corporates should navigate these trends and engage with ESG rating providers in this foreword from the latest Nordea On Your Mind, "ESG: Reaping the rewards."

In today's world, it is probably no understatement to say that sustainability has become the new normal. This certainly holds true in the financial markets, where the European Commission’s Action Plan on Sustainable Finance from 2018 has set off an avalanche of change. Much of this has been driven by policy and regulation. However, if we look to the private markets, arguably the most notable and strongest driver of sustainable finance, outside of the sustainable bond market perhaps, is the developments seen within ESG data services, including ESG ratings.

To get you properly caught up on these developments, let me take you through some of the key reflections to bear in mind when discussing these services and ratings. Let us start off with some obvious points:

- A lot of money is being thrown at ESG data/services: So much so that MSCI's ESG-focused business grew by +40% y/y in Q1 (versus 5-11% for its other businesses). Opimas has estimated 24% growth per annum since 2014 for ESG content and indices. With this much money chasing products, it is no surprise that companies are investing heavily in expanding their offerings.

- It is about more than just 'ESG ratings': In a world full of complexities and ambiguity, a simple rating is often the easiest to communicate. Naturally, we therefore see this as a cornerstone product of most ESG service providers – but it far from tells the full story. Most investors we speak to only use ESG ratings as a screening tool but rely on the fundamental ESG data for investment decisions.

- We need harmonisation of concepts but nuance in methodologies: To ensure that we are all on the same page, it is crucial that we harmonise our thinking around the nature of discussed concepts. One such example is regarding CO2 emissions, where the concept of "scope emissions" has taken hold and where the Science-Based Targets initiative has been driving the scientific agenda in aligning company targets. However, we still need to leave scope for different methodologies for how to apply such data, as sustainability discussions are inherently context-dependent, which is why it is often futile to compare ESG ratings across providers.

- Availability and quality of ESG data need to improve: Often these are raised as the primary concerns for the usage of ESG data and ratings – and to a certain extent, this holds true. However, we have seen significant progress in the last three to five years, especially for climate-related data, and we expect this development to drastically improve over the next three to five years, as both regulation and investor demand will drive companies to invest more time and effort into increasing and streamlining the reporting on non-financial data.

If we look more closely at the developments shaping the ESG service provider space, the first thing to recognise is the obvious structural driver, sustainability, as the new normal, as stated above. As a consequence of these strong tailwinds, we have seen a proliferation of service providers, but also industry consolidation. Indeed, we expect consolidation to be one of the main supporters of growth in the coming years as services become more harmonised. Interestingly, in the current market, we see three primary yet different providers/owners of ESG services, namely stock exchanges, credit rating agencies and research providers

Within the ESG service provider space, "ESG ratings" often represent the flagship product, probably because of their intuitive use and interpretation. However, it is important to recognise that the term "ESG ratings" is used quite ambiguously in the market today. Some providers refer to these as scores, others as assessments or evaluations, and some specifically as risk ratings. Inherent in these differences are different methodological assumptions and approaches. As an example, both MSCI and Sustainalytics base their ratings on an exposure risk and the company's ability to manage such risk. ISS ESG's approach is based on an overall ESG performance that is subsequently adjusted for the impact (positive or negative) of its products and services on the UN Sustainable Development Goals.

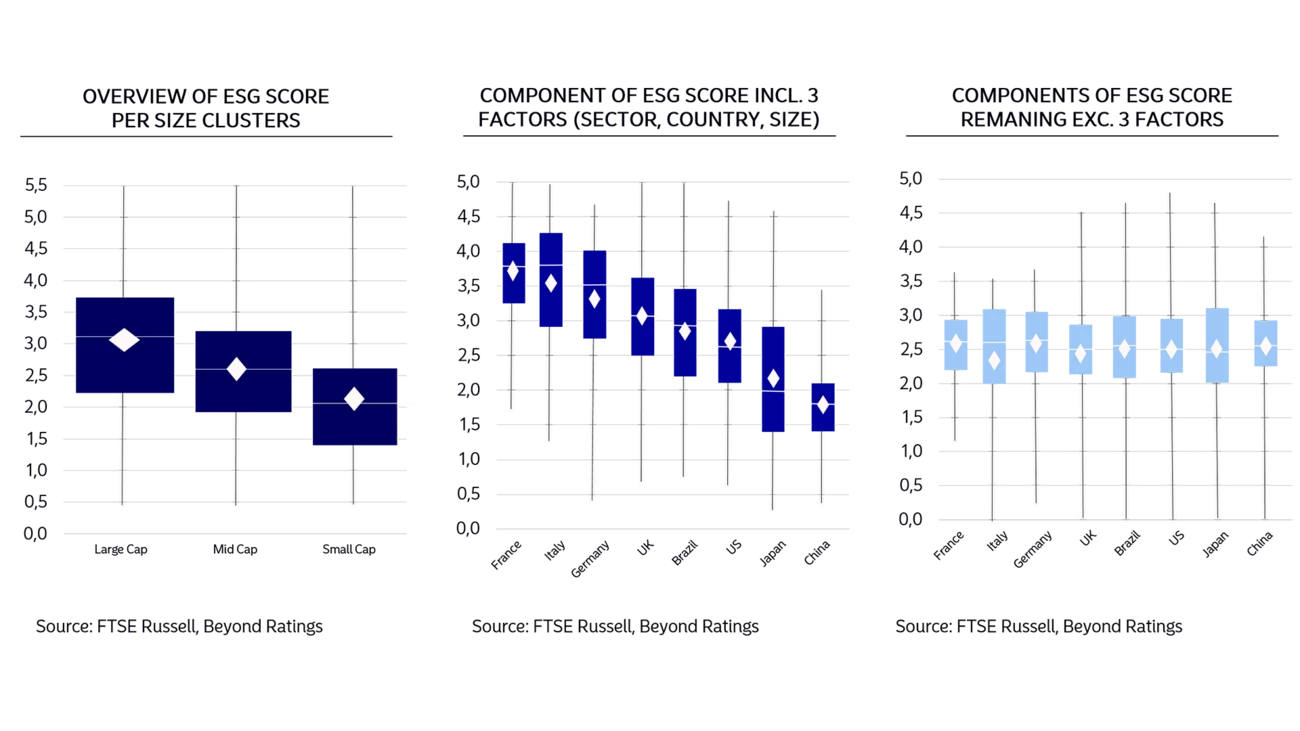

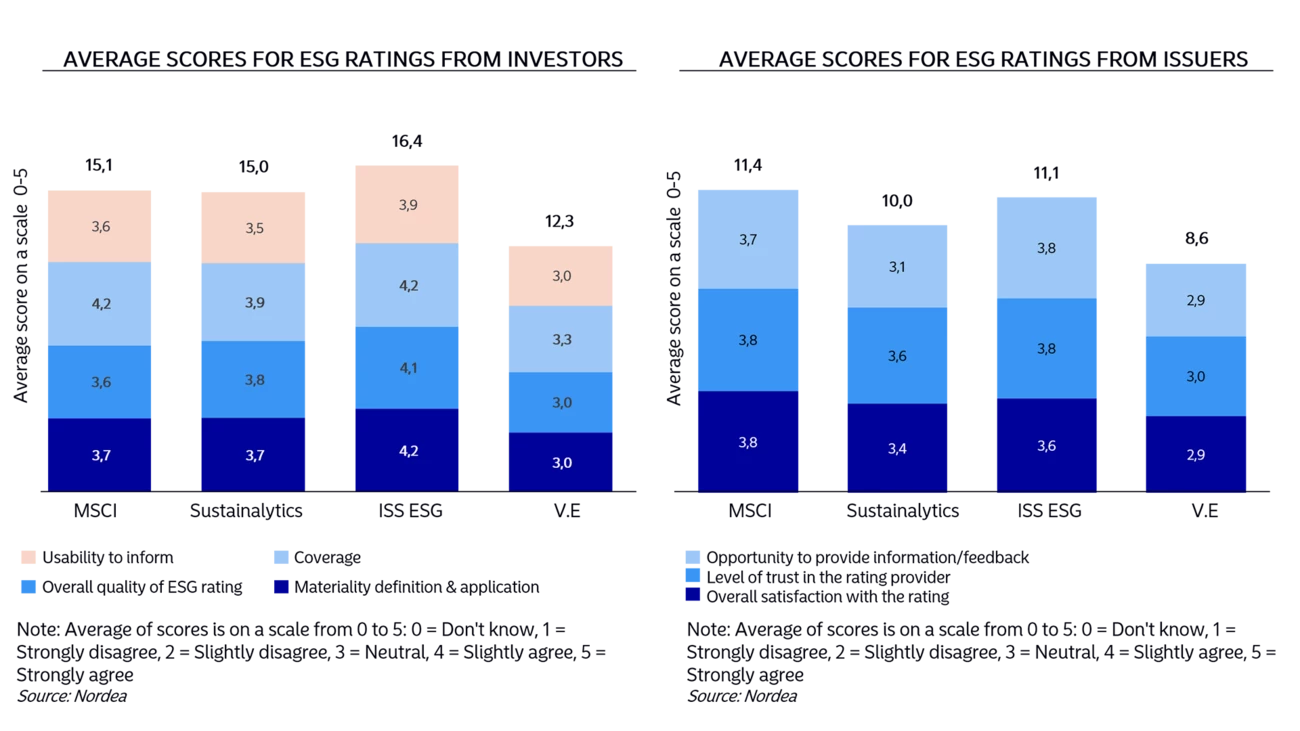

Regardless of the differences, the appetite for ESG ratings and ESG services more broadly is increasing dramatically – mainly from investors for support in investment decisions and alignment with responsible investment strategies, but also from corporates for support in strategy work and investor relations. However, it is important to be mindful of the inherent biases of these products and how they are used. Research by FTSE Russell and Beyond Ratings has shown that ESG ratings on larger companies or companies from certain countries include a positive bias (see figures above). When speaking to the more advanced investors, we are comforted by the fact that most of them tend to be aware of this, even if they do not adjust for it. Further, ESG ratings themselves are rarely used for investment decisions but rather for screening or relative value considerations. Also, from our recent ESG rating survey (see below), we found that there does not appear to be a meaningful difference in the quality of the services when adjusting for how well they are known.

What to be mindful of as a corporate when discussing ESG ratings internally:

- Make sure to answer the ESG questionnaires you get. And if there are too many, make sure to have a plan for how to optimise the time spent answering them.

- Be mindful of the fact that most service providers (and increasingly also investors) rely both on artificial intelligence (i.e. machine reading) and human intelligence (i.e. manual reading). Hence, your sustainability communication should address both needs – that is, data-heavy tables for machine reading, and simpler contextual infographics for people.

- Make sure to use "search-engine-optimisation" (SEO) techniques for your sustainability website so that your information and data is indexable and easily searched for on Google (let us not forget that this is still the main source of information even for advanced investors).

- A strong ESG rating is based on two components:

(i) A strong internal focus on actually improving the sustainability of the company

(ii) A clear plan for how to communicate the key sustainability aspects and data of your company. Barring any tangible sustainability improvements in the overall company, we strongly encourage companies to follow the developments on non-financial reporting, including voluntary initiatives such as the Task Force on Climate-related Financial Disclosures (TCFD) and the CDP as well. - Engage your trusted financial speaking partners for input on how to work with ESG ratings and data. At Nordea we stand ready.

Get the report

Top decision makers at Nordea’s large clients across the Nordic region receive Nordea On Your Mind around eight times per year.

If you are a corporate client and want to access the full Nordea On Your Mind report, please contact viktor.soneback [at] nordea.com (Viktor Sonebäck)

Sustainability

Nordic companies stick to climate goals despite global uncertainty

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

Read more

Sector insights

RESourceEU in the age of geoeconomics: Nordic companies positioned to seize opportunities

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

Read more

Open banking

How APIs power the real-time payments revolution in banking

The financial industry is right now in the middle of a paradigm shift as real-time payments become the norm rather than the exception. At the heart of this transformation are banking APIs (application programming interfaces) that enable instant, secure and programmable money movement.

Read more