How do we measure risk after a pandemic?

Sustainability isn’t just about the environment. Companies strive to be robust and able to take change in their stride. But few were prepared for a global pandemic on the scale of COVID-19. Businesses around the world were forced to shut their doors. Supply chains, sales models, and support services were all thrown up in the air.

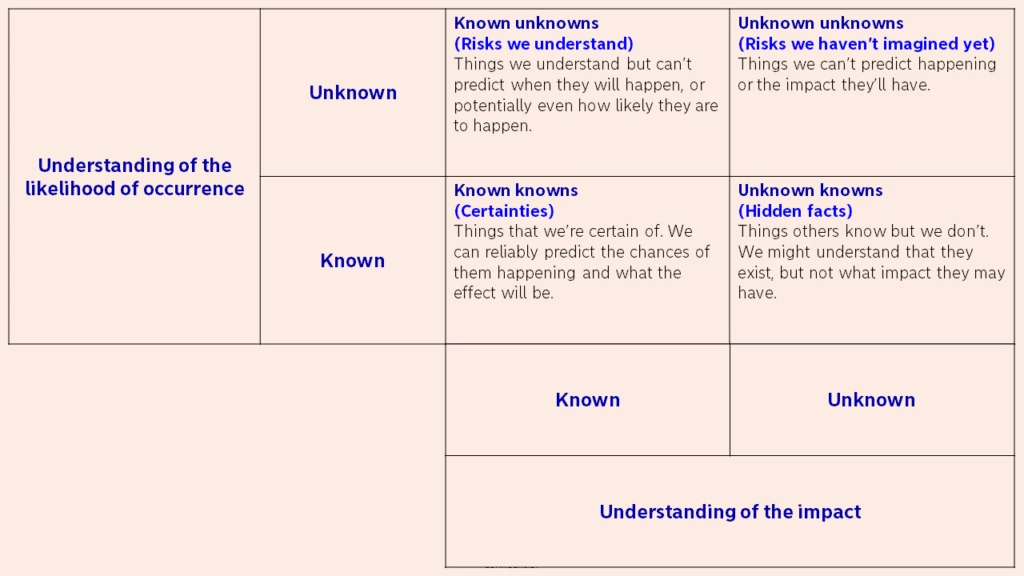

Understanding the risks

We’re living in unprecedented times. Traditional risk models did not account for a crisis on the scale of COVID-19.

We all knew that a pandemic could happen. They’ve been a staple for movies for years, but in real-life they always seemed so unlikely. There have been epidemics: swine flu, avian flu, Ebola, even outbreaks of measles in the US, but nothing on this scale.

COVID-19 exposed weaknesses in many company’s plans. Suddenly it wasn’t just about one site being disrupted, but hundreds of sites and often much of the supply chain. Few businesses were prepared for, or had even considered, what they would do in such a situation. The importance of speed was made clear as businesses were forced to adapt literally overnight.

So how can you prepare for something that you can’t predict? There are things we can predict, like the risk of a shipping container being lost at sea (about 0.0004%); we can even predict geopolitical events and extreme weather to a certain extent. What we can’t predict is something like COVID-19. We just don’t have the data. It’s these unknown unknowns that are hardest to plan for.

Protecting against the unknown

Insurance is likely to be one of the first things that springs to mind when you think about preparing for the unknown. Businesses will have a multitude of policies in place, often including cover for business interruption. But this is much more complicated than, say, car insurance. And that’s led to many disputes between insurers and policyholders over COVID-19. The scale of payouts is likely to be huge—Lloyds of London expects to pay out over £5 billion and incur significant losses. But even when payouts are made, they may be too late or too little to save many businesses.

Insurance is important, but it isn’t enough. To avoid disruption from future unknowns, businesses need increased agility, robustness and resilience. They need to be able to adapt quickly to whatever is thrown their way. When the lockdowns began, businesses that were more digital were able to cope better. They were able to pivot to home working and online sales and support in next to no time. Less advanced companies had more work to do.

COVID-19 has forced businesses to reconsider their business models and as a result, many have accelerated their digital transformation plans. Though this isn’t a situation any business wanted to be in, it is an opportunity for businesses to rethink how they operate and to make themselves stronger for the future.

Invest in your future

More digitally advanced businesses were enabled to respond to the COVID-19 pandemic more quickly. They were able to keep serving their customers by leveraging online channels and adapting their offerings. Many, especially those outside of retail and manufacturing, were able to keep office staff working from home with little impact on output. Adopting cloud-based applications and building online platforms can be an effective way for businesses to increase their adaptability and decrease their exposure to risks that cause disruption to transport or the use of facilities.

When crisis hits, businesses need access to capital to keep operating. When thousands of businesses are hit at the same time, borrowing money may not be easy or cheap. Cash management solutions can help. They can give visibility and control of cash flows and help manage risk. And they’re not just important in a crisis, they’re useful at any time to help businesses with their finances. Other strategies can help too, such as an FX risk management strategy — Nordea helped The Ball Group develop a strategy that saw it ride out the major currency volatility caused by COVID-19.

It’s likely that there will be future epidemics, but we can’t reliably predict whether there will be another global pandemic in our lifetimes, never mind the length of a company’s planning cycle. But it’s highly likely that you’ll face another crisis in your career.

Before COVID-19, PwC found that 70% of organisations had experienced at least one severe crisis in the preceding 5 years.[1]

Our ability to predict everything from floods to tornados, traffic jams to pandemics is likely to increase as artificial intelligence/machine learning (AI/ML) becomes more widespread. But there will always be risks that we cannot accurately predict. Resilience and sustainability should be an integral part of a company’s business model, not just a plan sitting on a dusty shelf.

Sustainable banking

Nordea recognised as climate transition leader in new Morningstar Sustainalytics report

Morningstar Sustainalytics has recently published a new report identifying companies that are taking steps to reduce emissions, set actionable targets and implement good governance practices. Nordea is highlighted for its significant progress in reducing emissions and its comprehensive climate targets.

Read more

Sustainability

Nordic companies stick to climate goals despite global uncertainty

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

Read more

Sector insights

RESourceEU in the age of geoeconomics: Nordic companies positioned to seize opportunities

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

Read more