Nordea On Your Mind is the flagship publication of Nordea Investment Banking’s Thematics team, which produces research for large corporate and institutional clients. The research does not contain investment advice and typically covers topics of a strategic and long-term nature, which can affect corporate financial performance. Top decision makers at Nordea’s large clients across the Nordic region receive Nordea On Your Mind around eight times per year. The publication’s themes vary widely, and many are selected from suggestions by clients. Examples of covered topics include artificial intelligence, wage inflation, M&A, e-commerce, income inequality, ESG, cybersecurity and corporate leverage.

Nordea On Your Mind

Capital markets discount a V-shaped recovery from COVID-19

What is driving the recovery amid ongoing uncertainty about the direction of the Covid-19 pandemic? Our Nordic Equity Strategist Arvid Böhm discusses this and other topics with Viktor Sonebäck of our Thematics Research team. The interview is part of the latest Nordea On Your Mind report, "Coronavirus: Plan B".

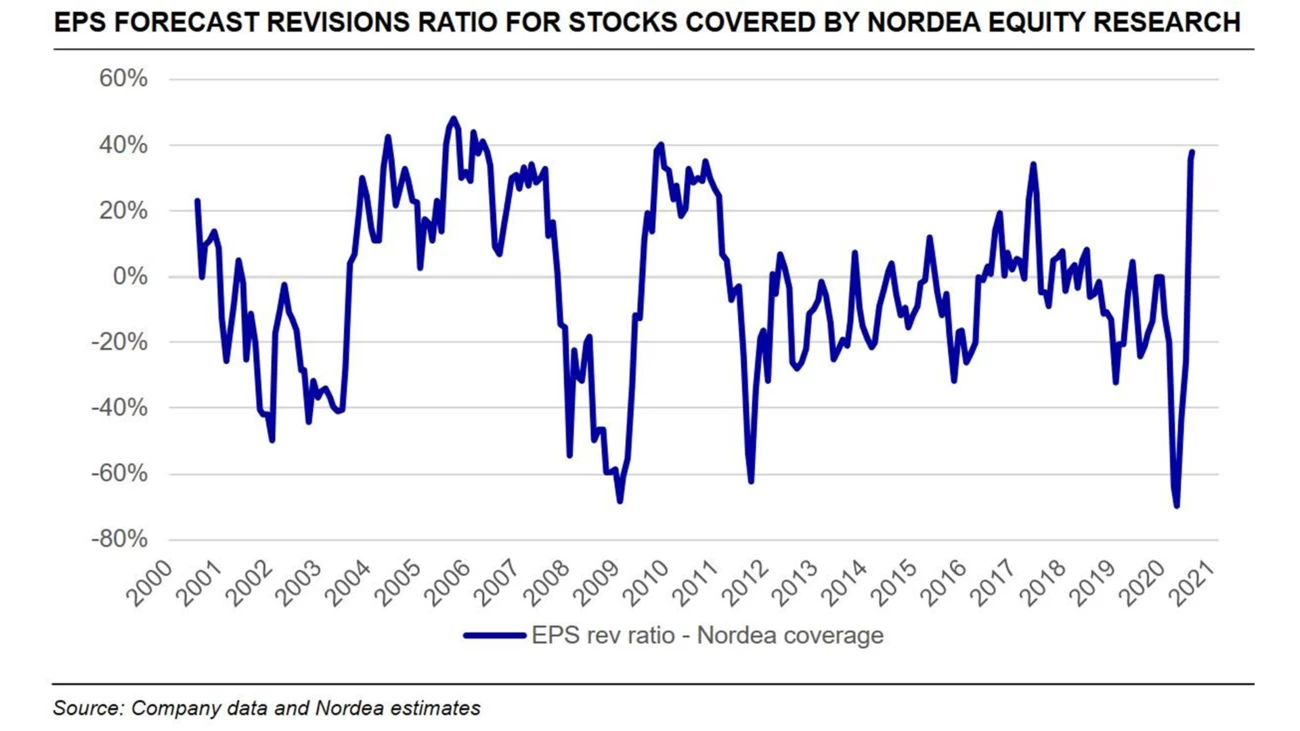

In the latest Nordea On Your Mind report "Coronavirus: Plan B", Viktor Sonebäck, Associate at Nordea Thematics, talked to Nordea's Nordic Equity Strategist Arvid Böhm (AB) about how Q2 interim reports were typically well received because expectations were lowered prior to their release - and how the ratio of upgrades to downgrades for EPS forecasts has turned positive.

Arvid Böhm elaborates on what kind of recovery is being forecast, and what is actually priced in by markets. We also discuss key factors for several scenarios, such as a vaccine or therapy development, and the potential stickiness of central bank and government stimuli.

Q2 interim reports from listed Nordic companies have given us a first impression of how they have been impacted by COVID-19 and associated lockdowns. How would you summarise the outcomes for the second quarter versus expectations, and how have the quarterly results and the outlook comments given by management been received by investors?

AB: In short, the Q2 reporting season saw profits falling off a cliff. However, as we approached the start of the Q2 earnings season, expectations had been reduced sharply. Calculated against the estimates for Q2 as we entered this year, Nordic adjusted EBIT estimates had been slashed by around 40%; but as it turns out, this was too much. The positive surprise has been massive, with the average EBIT being close to 20% better than expected. The market reaction, however, has been more tempered, and estimate revisions for the remainder of 2020 and 2021 as well. Actually, the market reaction on the day of the report has shown a strong correlation with profit revision for next year (2021), of around 1-1.5% on average.

Capital markets took a beating during the spring, with tanking equity indices and soaring corporate credit spreads. But capital markets have since recovered strongly. What is your impression of the key drivers behind this? Are investors more confident about underlying fundamentals recovering, or is it more driven by monetary stimuli such as central bank liquidity injections and low policy rates?

AB: I would argue that the key driver has been the extraordinarily large and unprecedentedly quick monetary and fiscal policy response to the economic shock that hit the economy. Furthermore, although it is a pandemic, acknowledging that it is a virus that normally eases both in terms of it spreading and how aggressive it is has calmed concerns. Part of the sharp market correction was also linked to the global lockdown of economies across the world in a synchronized manner. We have had little experience of this before. As lockdowns have started to be eased and government virus containment strategies are now seemingly more selective and concentrated, rather than broad and complete, a recovery from a total standstill could emerge and bolster investors’ confidence.

VS: Capital markets took a beating during the spring, with tanking equity indices and soaring corporate credit spreads. But capital markets have since recovered strongly. What is your impression of the key drivers behind this? Are investors more confident about underlying fundamentals recovering, or is it more driven by monetary stimuli such as central bank liquidity injections and low policy rates?

AB: I would argue that the key driver has been the extraordinarily large and unprecedentedly quick monetary and fiscal policy response to the economic shock that hit the economy. Furthermore, although it is a pandemic, acknowledging that it is a virus that normally eases both in terms of it spreading and how aggressive it is has calmed concerns. Part of the sharp market correction was also linked to the global lockdown of economies across the world in a synchronised manner. We have had little experience of this before. As lockdowns have started to be eased and government virus containment strategies are now seemingly more selective and concentrated, rather than broad and complete, a recovery from a total standstill could emerge and bolster investors’ confidence.

Arvid Böhm, Nordic Equity Strategist at Nordea

VS: What do you believe is the most critical data investors are watching for pricing equities? Clinical COVID-19 data, including vaccine and therapy development? Macroeconomic fundamentals? Corporate data? Government and central bank stimulus news? Other?

AB: I believe we are all watching all of these. Two of them, I would argue, are more critical, however. Should a renewed rise in virus spread (which is natural given that mobility restrictions are being eased) trigger governments to re-enter full lockdown strategies once again, I would expect market turmoil to come back. However, I would put a fairly low probability on this happening. The other is a vaccine. The amount of resources being allocated to achieving this is unheard of. We are not there yet, but I have confidence that we will get a vaccine and could possibly be looking at global distribution by the beginning of next year. Should that be the case, then we will be back at square one, before COVID-19 hit – with a few very important differences: pent-up demand, low inventories and massive fiscal and monetary policy in place. As history tells us, there is nothing as permanent as temporary policy measures, suggesting that policy schemes will be retracted with great hesitation.

VS: Ignoring differences between industry sectors and looking broadly, if I asked you to guess the probability of overall demand in the economy again reaching 2019 levels during 2021, what would you say?

AB: Given what I just said, I would argue that the probability of this happening has improved just over the last few months. It currently seems more likely than not. Certainly, renewed lockdown strategies and the world failing to create a potent and safe vaccine would clearly change this for the worse. The rise in unemployment would then risk gaining renewed momentum and larger pools of permanent unemployed being established. The funding sources for public support have been reduced and household savings would accelerate, shaving off the demand that is left even further.

Vaccine and/or therapy availability could bring the economy back to where it was in 2019 – with additional upside from pent-up demand, low inventories and massive policy support

Get the report

Top decision makers at Nordea’s large clients across the Nordic region receive Nordea On Your Mind around eight times per year.

If you are a corporate client and want to access the full Nordea On Your Mind report, please contact viktor.soneback [at] nordea.com (Viktor Sonebäck)

Sustainability

Nordic companies stick to climate goals despite global uncertainty

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

Read more

Sector insights

RESourceEU in the age of geoeconomics: Nordic companies positioned to seize opportunities

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

Read more

Open banking

How APIs power the real-time payments revolution in banking

The financial industry is right now in the middle of a paradigm shift as real-time payments become the norm rather than the exception. At the heart of this transformation are banking APIs (application programming interfaces) that enable instant, secure and programmable money movement.

Read more