- Name:

- Tuuli Koivu

- Title:

- Chief Economist

Helge J Pedersen , Tuuli Koivu

The Middle East war and the closure of the Strait of Hormuz disrupt energy and supply chains and weaken confidence. We therefore downgrade our global growth forecast, while central banks face rising price pressures.

The war in the Middle East has entered its third month and is now significantly impacting the global economy. The double blockade of the Strait of Hormuz has caused sharply higher energy prices and extended delivery times for many raw materials and semi‑finished goods. Inflation is increasing, and weaker confidence indicators are reported among both households and businesses worldwide. Against this backdrop, we have revised down our global economic forecast for this year to 3.1% from 3.3% in January, while slightly upgrading our forecast for next year from 3.2% to 3.3%.

In the baseline scenario, we anticipate some reopening of the Strait of Hormuz in the coming months, although at least some problems are likely to persist and even a large‑scale energy crisis cannot be ruled out. The approaching US midterm elections may influence peace negotiations between Iran and the US administration. Meanwhile, oil futures pricing—an external assumption for inflation and growth forecasts—is trending rather steeply downward. The Russian assault on Ukraine is likely to continue, and geopolitical risks remain elevated.

Among major economies, the euro area appears the most vulnerable to these shocks due to its heavy dependence on imported fossil energy. Conversely, the energy balance has improved in the US, while in China price controls and large stockpiles imply slower pass‑through effects from higher energy prices.

Central banks face increasingly complex challenges as price pressures drive up inflation. Crucially, these pressures extend beyond energy, since the Middle East plays a key role in global supply chains for, for example, food, semiconductors, and many metals. Consequently, central banks have begun to worry about broader‑based inflationary pressures, already reflected in higher market interest rates.

Table: GDP growth forecast, % Y/Y

| Year | World New | World Old | US New | US Old | Euro area New | Euro area Old | China New | China Old |

|---|---|---|---|---|---|---|---|---|

| 2024 | 3.4 | 3.4 | 2.8 | 2.8 | 0.7 | 0.7 | 5.0 | 5.0 |

| 2025E | 3.5 | 3.3 | 2.1 | 2.2 | 1.5 | 1.5 | 5.0 | 5.0 |

| 2026E | 3.1 | 3.3 | 2.3 | 2.3 | 1.0 | 1.5 | 4.5 | 4.5 |

| 2027E | 3.3 | 3.2 | 2.1 | 2.0 | 1.5 | 2.0 | 4.0 | 4.0 |

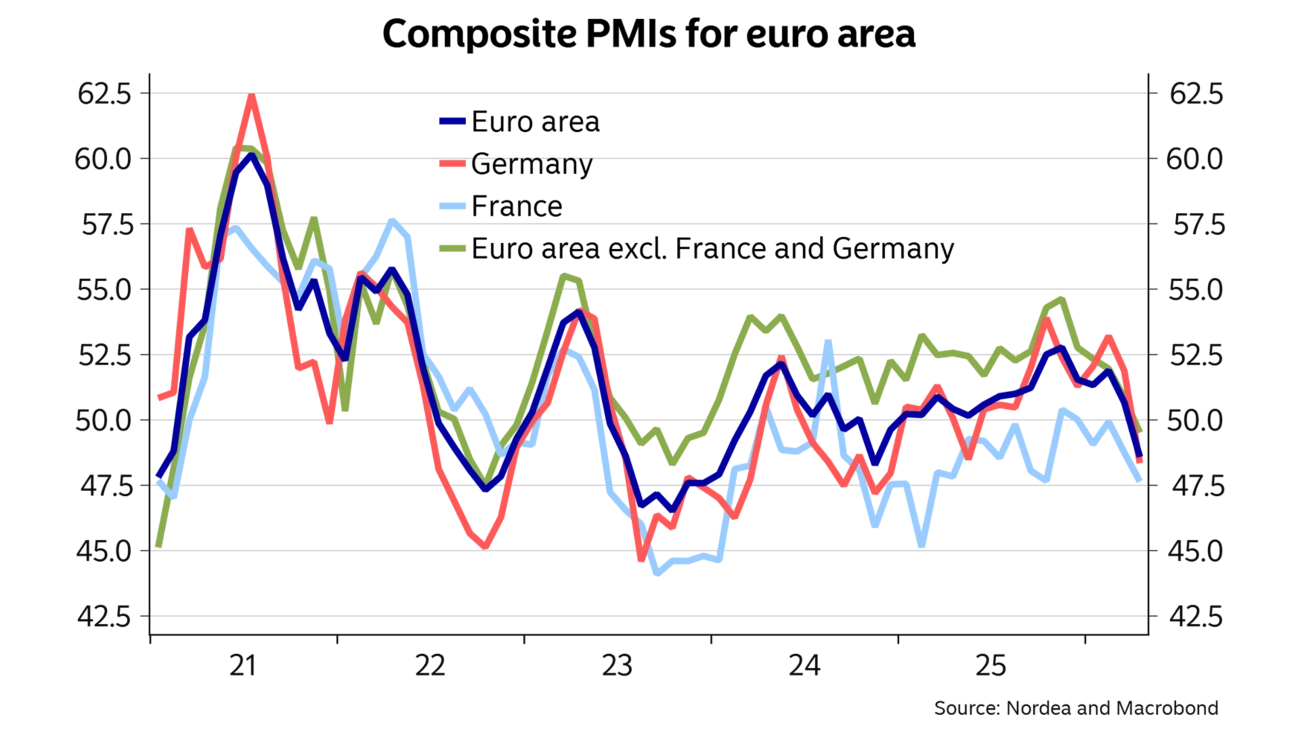

As noted, the euro area remains dependent on imported energy and critical bottlenecks in certain types of deliveries may become highly visible already in the coming months. Thus, the euro-area growth outlook is vulnerable to problems in international energy markets and higher energy prices. Recent PMI and consumer confidence data indicate that the coming months are likely to be challenging, due to a smaller‑than‑expected increase in consumers’ purchasing power and elevated concerns over global supply chains. Consequently, we have revised our euro‑area GDP forecast down by half a percentage point for both 2026 and 2027, to 1.0% and 1.5%, respectively.

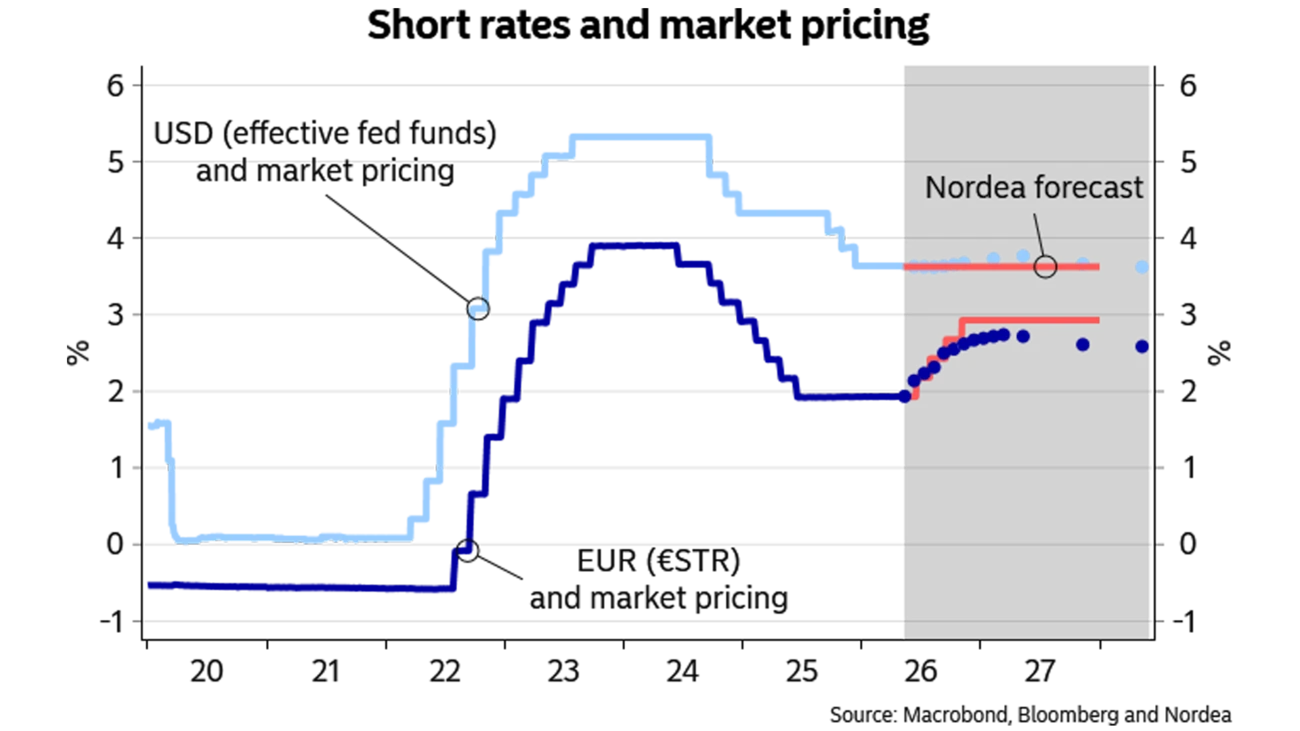

The downward revision for 2027 partly reflects our updated ECB forecast, which assumes that the central bank will raise policy rates by a full percentage point by the end of the year. We expect rate hikes to start in June, driven by price pressures that companies are increasingly signalling. Some of the pressures were already visible in some sectors prior to the war and according to the survey indicators, are now spreading from manufacturing to services.

It is important to keep in mind that, from a euro‑area growth perspective, there are also important differences between the current situation and the period following Russia’s invasion of Ukraine. Europe’s direct dependence on Gulf‑produced energy is lower than its reliance on Russian energy in 2022, and confidence effects among consumers have so far been more limited. Moreover, the ECB’s response to the inflation shock is expected to be much smaller this time. As a result, the prolonged period of near‑zero growth experienced in the euro area in 2023–2024 may not be repeated although the risks around our GDP forecast are clearly biased to the downside.

Central banks face increasingly complex challenges as price pressures drive up inflation.

The US economy continued to grow at a steady pace in the first quarter of 2026, with GDP increasing at an annual rate of 2%. In particular, an acceleration in investment, government spending, and net exports contributed to this outcome, while household consumption growth slowed as real income growth remained subdued due to relatively high inflation, slower employment growth, and more moderate wage increases. We nevertheless maintain a relatively benign view of the economy and expect it to grow by around 2% this year and next.

We continue to expect the Fed to keep policy rates unchanged this year and next. Alongside higher inflation readings, market pricing has moved to match closely our forecast and the expectations of rate cuts have vanished. The end of Jerome Powell’s term as Fed Chair is likely to have only a limited impact on the rate path as concerns regarding the Fed’s independence have eased since our previous forecast round.

China’s official first‑quarter growth data indicate that the economy is on track to meet its 2026 growth target of 4.5–5.0%. Growth continues to rely heavily on exports, which increased by 12% year‑on‑year in January–March, highlighting China’s exceptionally strong competitiveness across many sectors. In particular, exports of semiconductors, other high‑tech electronic products, and electric vehicles have surged.

The outlook for consumption is stable but moderate. While consumption is growing, momentum remains constrained by weak labour and housing markets, which are unlikely to strengthen meaningfully in the near term. Neither the 2026 budget nor the new five‑year plan appears to allocate significant resources to supporting household demand, and we expect Chinese households to remain cautious.

At the same time, policy priorities focused on self‑sufficiency, innovation, and the adoption of new technologies—including in traditional industries—are likely to support the supply side of the economy. Consequently, the low wage pressures and the problem of overcapacity are expected to keep price pressures contained, allowing China’s export sector to remain extremely competitive. Together with limited access for foreign companies to Chinese markets, this is likely to keep China’s trade surplus at elevated levels and to intensify criticism of China’s economic policy. As a result, the debate over China’s access to the EU market is likely to intensify, and President Trump’s visit to Beijing, rescheduled for mid‑May, will be closely watched.

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Economic Outlook

The Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

Read more

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Economic Outlook

The Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

Read more

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more