Watch the webinar

Get the economic outlook for Denmark directly from our economists in this on-demand webinar (in Danish).

See the webinarDenne siden findes ikke på norsk

Bli værende på denne siden | Fortsett til en lignende side på norskThe war in the Middle East challenges the resilience of international and Danish economies, but the foundation for continued growth is quite solid.

The war in the Middle East has entered its third month and is now significantly affecting the global economy. The double blockade of the Strait of Hormuz has caused markedly higher energy prices and extended delivery times for many raw materials and semi-finished products. Inflation is rising, and weaker confidence indicators are being reported among both households and businesses worldwide. Against this backdrop, we have revised our forecast for global economic growth this year slightly down to 3.1% from 3.3% in January, while we have upgraded the forecast for next year to 3.3% from 3.2%.

Among the major economies, the eurozone appears most vulnerable to these shocks due to its heavy dependence on imported fossil energy. Conversely, the energy balance has improved in the US, while price controls and large inventories in China imply a slower transmission from higher energy prices. Central banks face increasingly complex challenges as growth declines while price pressure drives inflation up. It is crucial that this inflationary pressure is not only about energy, as the Middle East also plays a key role in global supply chains for, for example, food, semiconductors, and many metals. As a result, central banks have begun to worry about broader-based inflationary pressure, which is already reflected in higher market rates. Read more in our Global Update: Geopolitical drag.

In the baseline scenario, we expect some reopening of the Strait of Hormuz in the coming months, although the situation is complicated and even a large-scale energy crisis cannot be ruled out. The upcoming US midterm elections may affect peace negotiations between Iran and the US administration. We use oil futures prices as an exogenous assumption for inflation and growth forecasts. At the time of writing, they show a rather marked decline over the coming years. The Russian attack on Ukraine will likely continue and geopolitical risks are assumed to remain high.

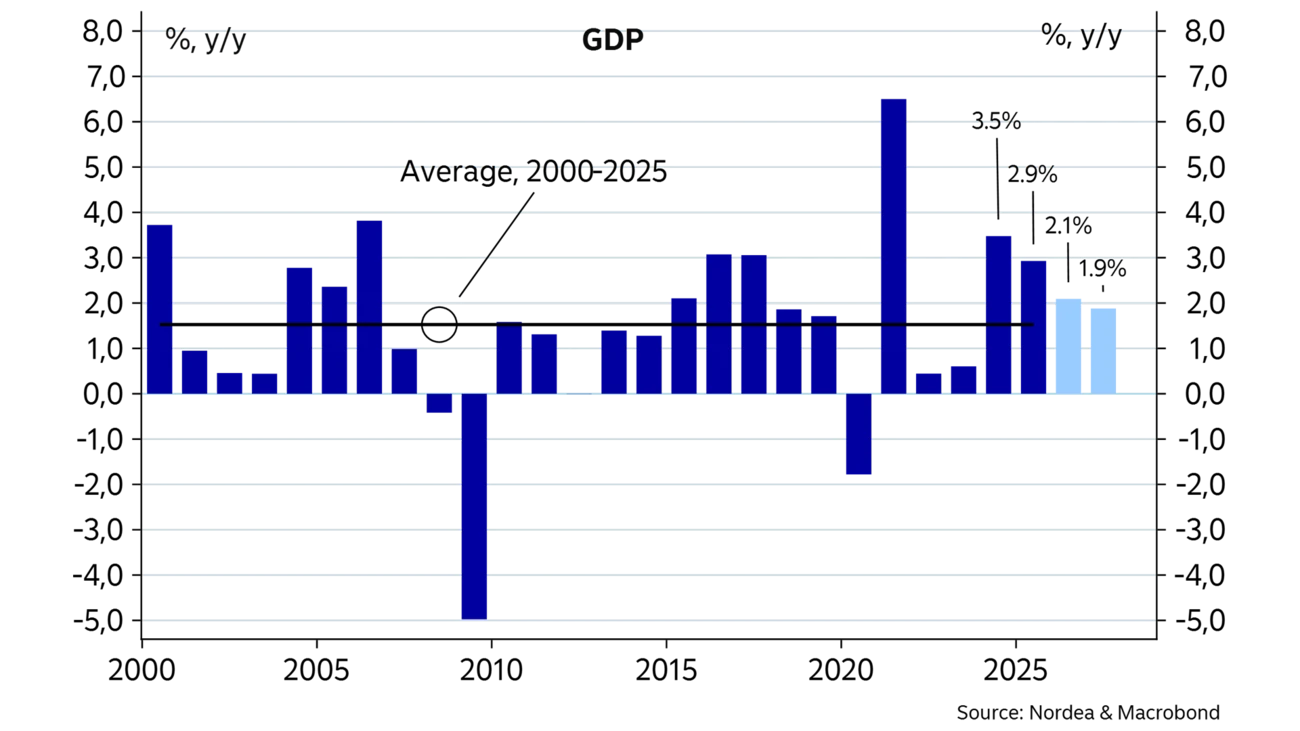

The Danish economy came out of 2025 at a very high activity level. This has long-lasting effects in 2026, where the Danish economy as a whole is expected to grow by 2.1%. This would be the third consecutive year with economic growth above 2%, we note. This is a downward adjustment compared to our forecast from January, where we expected growth of 2.5%. Conversely, however, it will still be more than double our growth expectations for the eurozone. For next year, we maintain the forecast of 1.9% growth in the Danish economy.

Despite the strong starting point, smaller cracks have recently appeared in the strong foundation. The value of Danish goods exports to the US has decreasedin the first quarter of the year. At the same time, observations from the labour market show that employment has stagnated, and unemployment is rising slightly – although some of this could be explained by the harsh winter. Overall, this points to the Danish economy heading into a period with more subdued growth than in previous years.

Tax cuts have provided solid support to household purchasing power from the beginning of the year. This has indeed led to higher activity in retail stores and increased car sales. However, the growth in consumption has been limited by continued high savings. The low consumption appetite is also expressed in consumer confidence measurements, which are far below the historical average. Here, it is especially households' assessment of future prospects that is a drag. This applies both to the assessment of the family's own situation and to the perception of the Danish economy.

Despite the current challenges, we maintain our expectations that private consumption will be a significant catalyst for growth over the coming years. In this light, we expect annual growth in private consumption of around 2% for both 2026 and 2027. Even stronger growth is expected in public consumption. This is especially due to the large increase in defence spending, which is planned to constitute 3.5% of GDP. However, there is great uncertainty about how and when the increased resources for defence will be converted into actual consumption and investments.

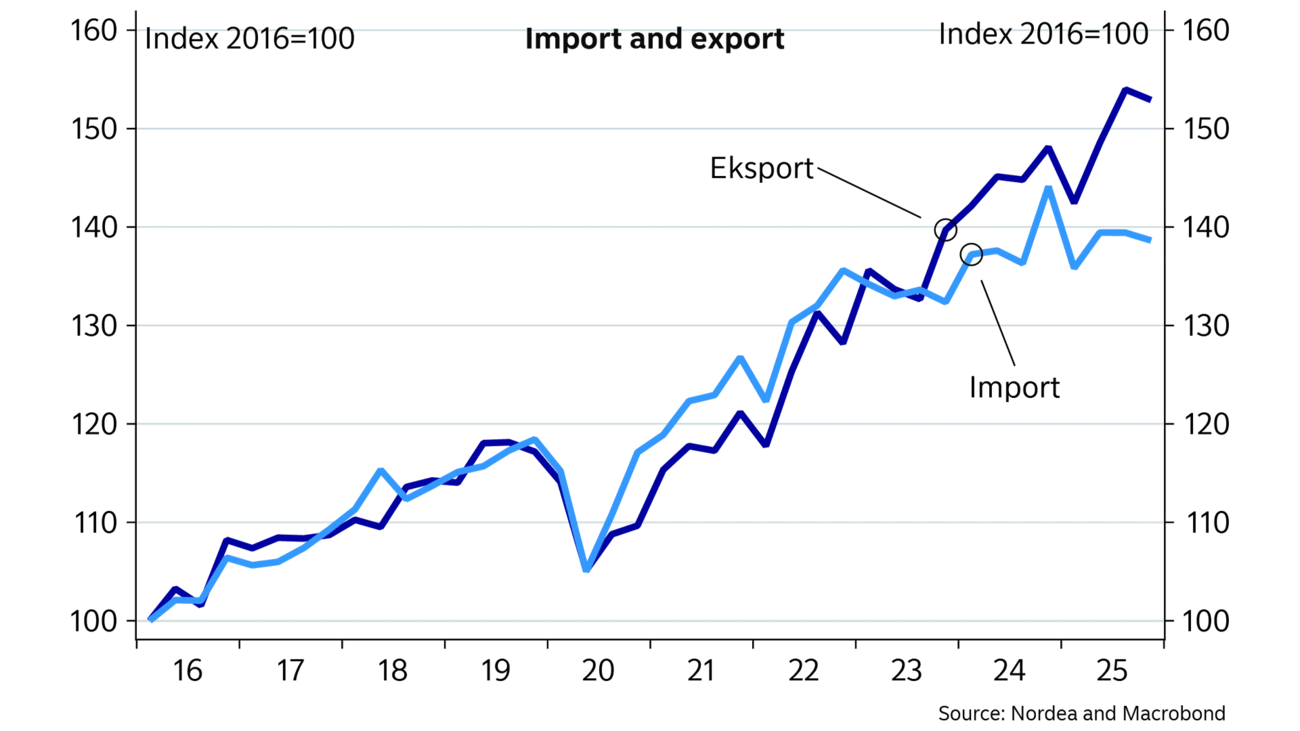

Over the past three years, the high growth in net exports has been the most important contributor to overall growth in the Danish economy. Here, especially a marked growth within the pharmaceutical industry has been a decisive factor.

This contribution is expected to gradually decrease over the coming years, although there is still the prospect of a large surplus on the balance of payments. Export growth will be challenged by downward-adjusted growth expectations for the eurozone and by the marked increases in tariff rates on imported goods to the US. This will affect companies negatively even though a large part of exports today are produced outside Denmark's borders. Conversely, imports to Denmark are expected to grow in line with higher consumption in both the public and private sectors.

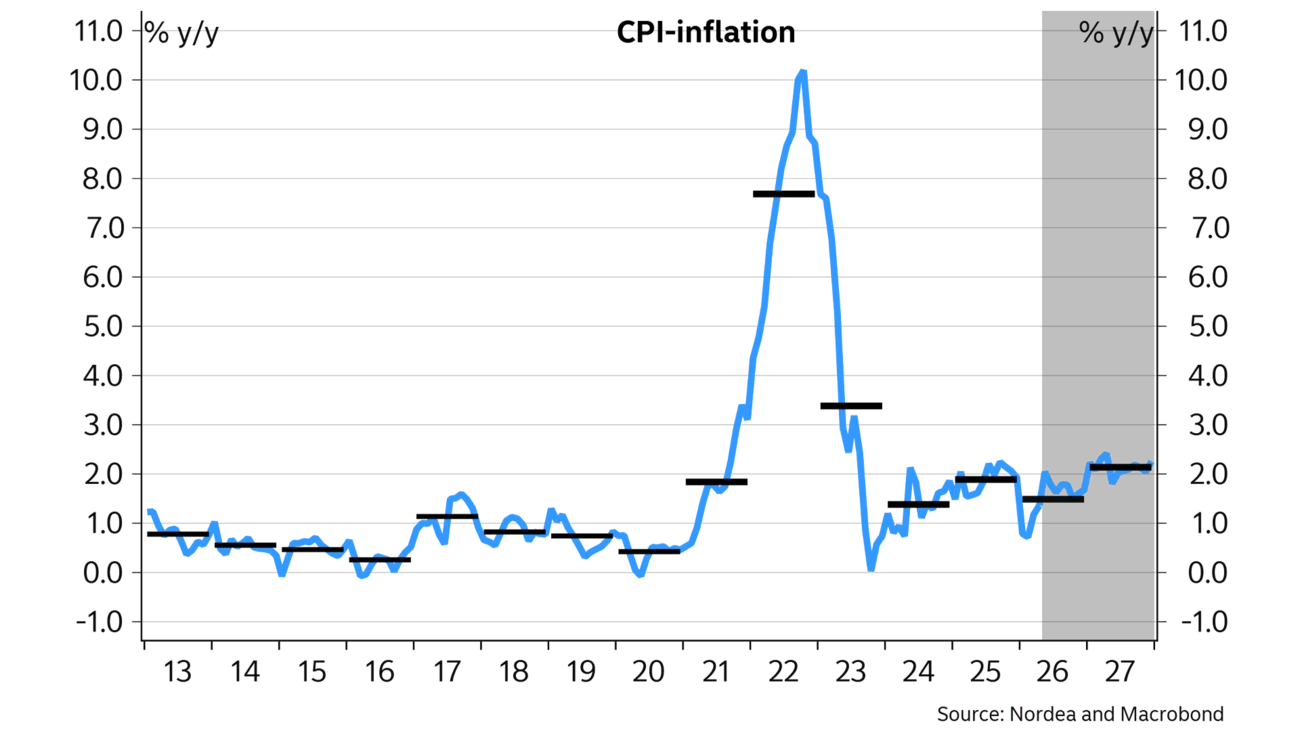

Since the beginning of the year, inflation in Denmark has been markedly below the level in surrounding countries. This is especially due to the decision to reduce the electricity tax to the EU's minimum limit. This has meant that Denmark is currently the EU country with the lowest inflation.

Although the starting point for inflation is low, Danish consumer prices are not isolated from global events. Thus, the annual growth rate in consumer prices has doubled since February. The increase has been driven by markedly higher prices on gasoline and diesel in particular. In addition, higher rents are also contributing to higher inflation.

We expect inflation to rise further over the coming months as the effects from higher energy prices spread like ripples in water. Overall, the average inflation this year is expected to land at 1.5%, which is slightly lower than the average in 2025. If the electricity tax had not been reduced, inflation would probably be above 2% this year. For next year, we expect the average inflation to rise to 2.2%.

For both years, the expected rise in consumer prices is below the forecast for wage development. Thus, there is a prospect that wage earners will experience continued growth in purchasing power.

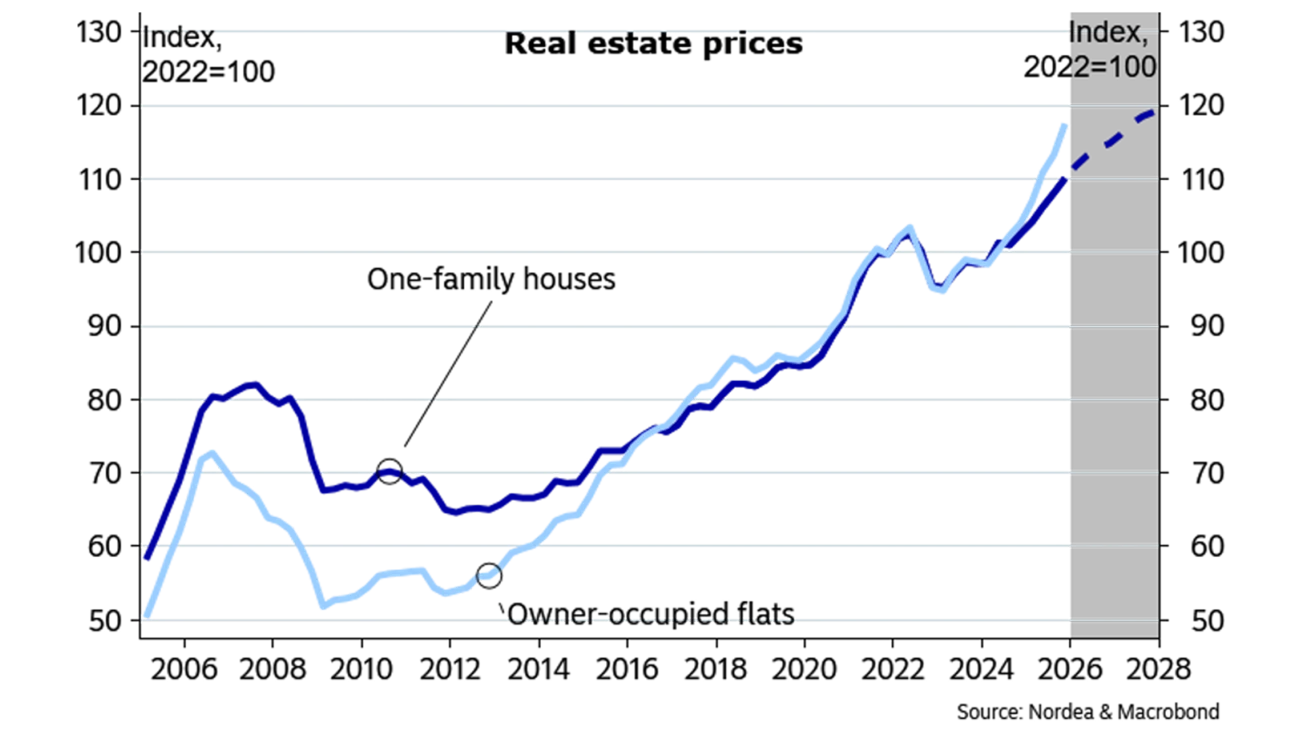

Like the rest of the Danish economy, the housing market has been at full speed in recent years. Since the beginning of 2024, the average square meter price for single-family houses has risen by more than 10%. Even larger price increases have occurred in the market for condominiums, where sales prices have risen by 20% in the same period. The rising housing prices have been driven by a combination of continued growth in employment and a low number of homes for sale. This especially applies in the capital area, where sales prices have risen the fastest.

We expect the progress in the housing market to continue towards the end of next year. However, slightly higher interest rates and a larger supply of homes for sale are expected to limit the pace somewhat. In this light, we expect average sales prices to rise by 6% this year and just under 4% in 2027.

The Danish krone has traded above the central parity against the euro for an extended period. However, the weakening has not yet been so strong that it has been necessary for the National Bank to intervene in the foreign exchange market.

Given a large foreign exchange reserve of almost DKK 700bn (approximately 21% of GDP), we assess that even if the National Bank begins to intervene in the foreign exchange market, there is still a long way to an independent Danish interest rate increase. Therefore, we also have as our main scenario that the interest rate differential to the eurozone will be maintained at 0.4 percentage points towards the end of next year.

Get the economic outlook for Denmark directly from our economists in this on-demand webinar (in Danish).

See the webinar

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Economic Outlook

The Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

Read more

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more