- Name:

- Juho Kostiainen

- Title:

- Nordea Economist

The Finnish economy is headed towards a mild recession this winter, but for the full year we fore-cast zero growth. Consumer purchasing power is constrained at the moment, but easing inflation and rising salaries will boost private consumption towards the end of the year. House prices are expected to continue falling in the first half of this year as the housing market seeks a new balance amid higher interest rates.

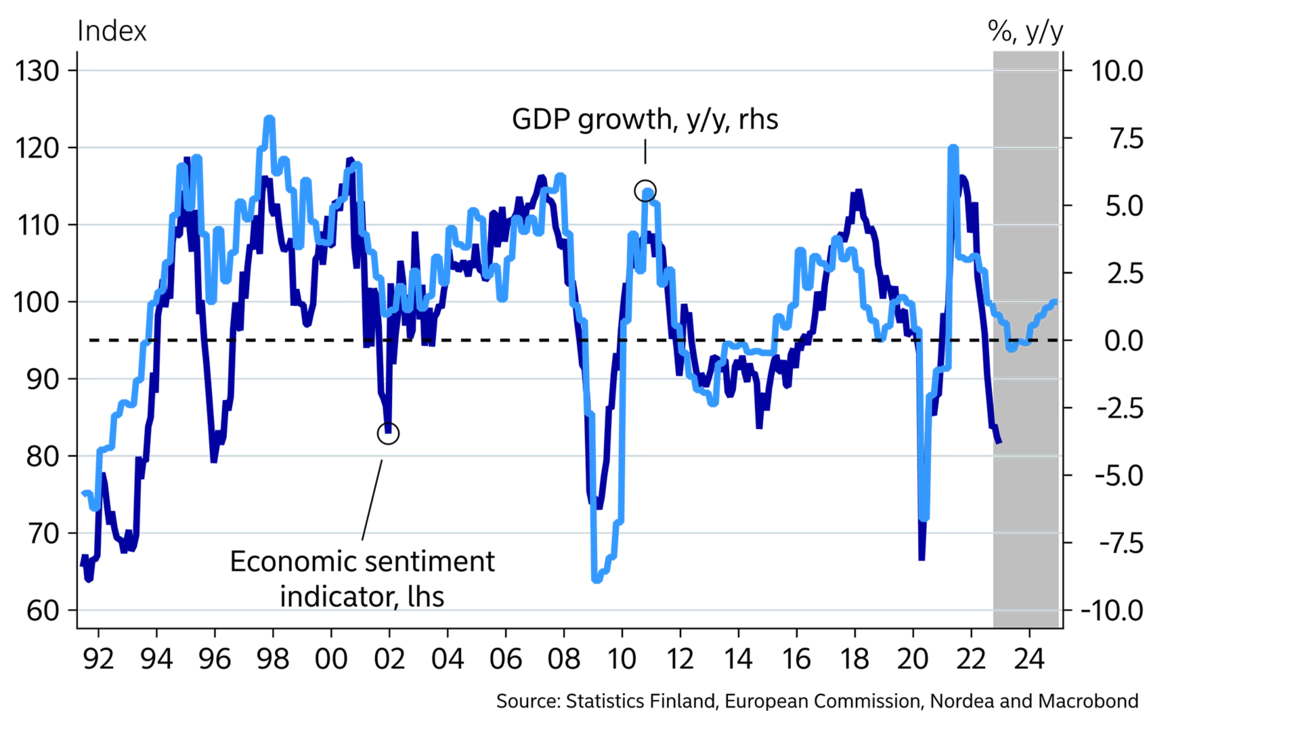

The Finnish economy recovered quickly at the start of last year following the lifting of COVID restrictions and driven by global economic growth. The employment situation also improved rapidly, pushing the unemployment rate below 7%. However, growth began to slow down towards the end of 2022. GDP contracted slightly (-0.2% q/q) in the third quarter, as a sharp rise in prices and interest rates dampened private consumption by weakening consumer purchasing power.

The rapid rise in interest rates and weak consumer confidence have also been reflected by the housing market, where demand died down and prices began to fall. This will clearly decelerate residential construction this year. The slowdown in global economic growth is beginning to show in dwindling demand for exports and a decline in export prices.

The economic outlook for this year is very mixed. Consumer and corporate confidence in the economy is bleak, resulting in increased caution with larger acquisitions and investments. On the other hand, energy prices are falling and inflationary pressures caused by bottlenecks in global supply are easing, which will provide relief for household finances towards the end of the year. Employment is expected to decline only moderately, supporting economic activity. The outlook for the European economy is brighter, too, as the worst scenarios involving an energy shortage do not appear to be materialising this winter.

We forecast that GDP will contract moderately in the first half of the year, only to return to a growth track in the second half. We expect GDP growth to be zero for the full year of 2023. As for next year, we forecast scant GDP growth of 1%.

Consumers will be tested this winter. The high cost of electricity, a rapid rise in interest rates and higher prices in many products and services pushed head-line inflation to as much as 9.1% in December. Wage increases, on the other hand, were less than 3% last year, which means consumer purchasing power has shrunk considerably.

However, the outlook going forward is more favourable for the consumer. Wages are expected to increase by 4% this year. Meanwhile, the price of electricity is expected to become more moderate, and government subsidies will bring relief to those struggling with large electricity bills.

Overall, inflation is expected to clearly fall this year as, along with energy, transportation costs have come down and bottlenecks in global production chains have eased. Full-year inflation is expected to be 5%, falling further to 1.7% in 2024.

As for interest rates, the situation doesn’t look to be easing this year, with the 12-month Euribor expected to be over 3% at the end of the year. This means that households’ interest expenses will increase from the current 2% up to 5% of their income.

|

|

2020 |

2021 |

2022E |

2023E |

2024E |

|

Real GDP, % y/y |

-2,4 |

3,0 |

2,0 |

0,0 |

1,0 |

|

Consumer prices, % y/y |

0,3 |

2,2 |

7,1 |

5,0 |

1,7 |

|

Unemployment rate, % |

7,8 |

7,6 |

6,8 |

7,0 |

7,0 |

|

Wages, % y/y |

2,0 |

2,4 |

2,6 |

4,0 |

3,4 |

|

Public sector surplus, % of GDP |

-5,5 |

-2,8 |

-1,80 |

-1,3 |

-1,8 |

|

Public sector debt, % of GDP |

74,8 |

72,4 |

71,4 |

70,5 |

71,1 |

|

ECB deposit interest rate (at year-end) |

-0,50 |

-0,50 |

2,00 |

3,25 |

2,50 |

Consumer purchasing power began to deteriorate in the latter half of last year, causing private consumption to decline slightly. In particular, the trade in goods suffered from weaker purchasing power and the decrease in goods consumption from the pandemic period. Demand for services remained strong last year, with service consumption recovering to its normal level. The latest card payment statistics, however, indicate that growth in service consumption is also abating.

Private consumption is expected to shrink moderately in the first half of the year, as price inflation continues to outpace wage growth. However, consumers still have a considerable amount of savings from the COVID years that they will spend to maintain their lifestyle even with higher prices, which will mitigate the drop in consumption. The decrease in private consumption is expected to turn to growth in the second half of the year, when lower inflation and higher wages begin to boost purchasing power.

In fact, the decline in real wages is expected to come to an end this year, and next year we will revert back to normal, with wages rising faster than prices.

The employment rate topped 74% last year, and many sectors have struggled with labour shortages. The in-crease in total working hours, however, has been much slower than the growth in employment because part-time jobs have contributed considerably to this growth. Employment remained strong late last year even though the general economic conditions began to deteriorate. The number of job vacancies has nonetheless begun to decrease, indicating that the period of rapid expansion in the labour market is over.

Weaker economic growth is expected to result in a moderate increase in unemployment this year. The construction sector, in particular, faces a clearly deteriorating outlook, although the large proportion of foreign labour in this sector will soften its impact on unemployment in Finland. The unemployment rate is expected to rise to 7% this year.

Consumer purchasing power will recover next year.

Industrial production has made it relatively unscathed through the waves of the pandemic and the sudden halt in trade with Russia. In fact, strong global demand and the rise in prices helped many export companies achieve strong profits last year. However, the growth spurt in the manufacturing sector is losing steam, and the number of new orders has decreased as global demand has levelled off.

Finland’s goods exports grew last year despite the complete stop in trade with Russia. Strong order books helped compensate for the closure of the Russian export market, buoying exports throughout 2022. The flow of new orders has dwindled, putting exporters in a more challenging situation this year, as demand has decreased both in Europe and in the US. The lifting of COVID restrictions in China and the subsequent recovery of its economy will add a much needed boost to the global economy. Goods exports will grow only slightly this year, though.

Finland’s current account was clearly negative last year. The balance on services, in particular, has weakened considerably, as overseas travel by Finns has recovered much faster than the tourist industry in Finland. The growth in service exports, however, is expected to continue at a relatively good pace this year. The balance on goods has also turned negative, which is explained by the sharp rise in imported energy, in particular.

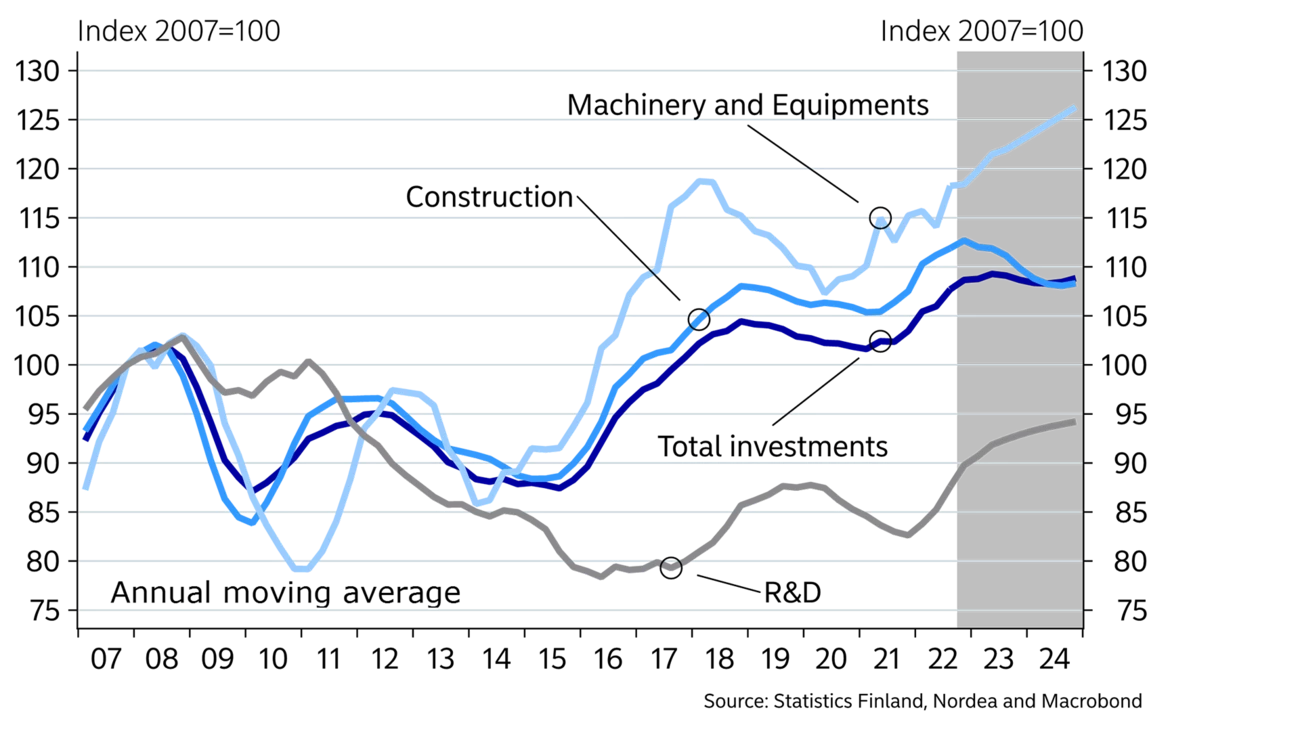

There was broad-based growth in investments in 2022, amounting to about 5% year-on-year. Residential construction was very brisk, and good demand in the man-ufacturing sector as well as renewable energy projects boosted investment in machinery and equipment. Moreover, investments in research and development began to clearly grow for the first time in a long time.

Residential building permits and new construction starts began to decrease at the end of last year as the housing market slowed down. This will result in less construction this year once ongoing projects are completed. In 2024, construction is expected to be even more sluggish than this year, despite the costs of construction beginning to fall thanks to cheaper materials.

In the manufacturing sector, the decrease in the capacity utilisation rate will reduce the need for investment, but on the other hand, investments in energy efficiency and clean energy will continue to feed growth in manufacturing investment this year. The construction of wind power will continue to be brisk. Relatively cheap and clean electricity generation is now attracting new types of green transition investments in Finland since many other European countries are still lagging far behind in their transition to clean energy.

House prices are seeking a new balance amid higher interest rates.

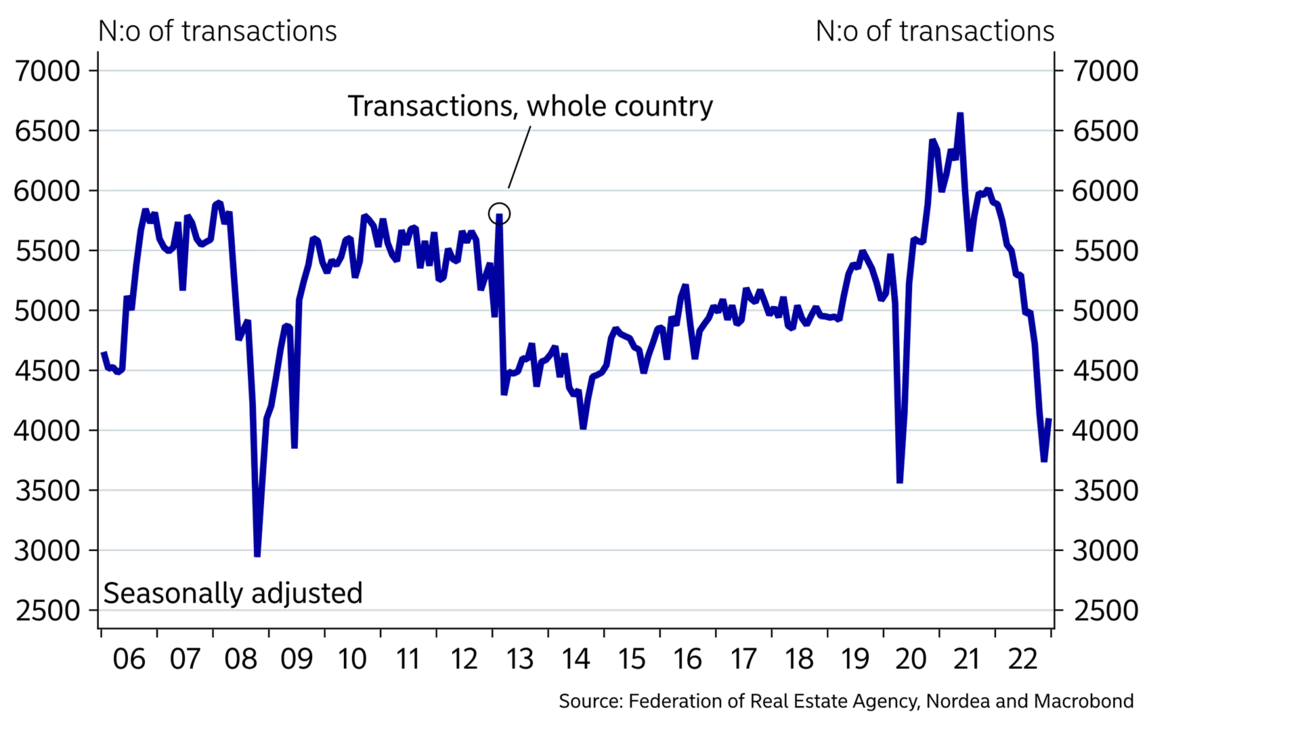

Housing sales decreased significantly at the end of last year as interest rates rose rapidly. House prices have also begun to drop. Year-on-year, the prices of old apartments have decreased by 3.4% across Finland and by 5% in the largest cities.

House prices are expected to continue falling in the first half of this year as the housing market seeks a new balance in a higher interest rate environment. We forecast that house prices will decrease by another 5% this year on average across the country. The employment situation, interest rates and general confidence in the economy will be crucial in order for the housing market to stabilise. The market is expected to return to normal after a weak start to this year once the rise in interest rates slows down and household finances improve due to lower inflation.

There has been plenty of oversupply in the rental market in recent years because the construction of rental apartments has outstripped demand. As a result, rents have increased quite moderately even though housing maintenance charges and interest expenses have risen relatively rapidly. Investor interest in the housing market has clearly decreased, as returns are lost on higher costs while rents remain practically unchanged. This has been reflected in a sharper-than-average drop in the prices of small apartments.

Finland’s public finances stabilised considerably last year. Tax revenues grew strongly as the economy recovered from the pandemic and prices increased in general. The public sector deficit fell to 1% of GDP last year. However, government debt continued to increase rapidly last year, even though the debt-to-GDP ratio remained stable on the back of rapid nominal GDP growth.

The outlook for the public finances for this year and next is clearly gloomier than last year’s because public spending is set to grow rapidly due to higher inflation and wage increases. In addition, many discretionary expenses, such as energy subsidies and military spending, will expand the deficit this year. We delve into the outlook for the public finances in more detail in our Finland Economic Outlook theme article.

This article first appeared in the Nordea Economic Outlook: The balancing act, published on 25 January 2023. Read more from the latest Nordea Economic Outlook.

Corporate insights

Despite global uncertainties, Sweden’s robust economic fundamentals pave the way for an increase in corporate transaction activity in the second half of 2025. Nordea’s view is that interest rates are likely to remain low, and our experts accordingly expect a pickup in deals.

Read more

Economic Outlook

Finland’s economic growth has been delayed this year. Economic fundamentals have improved, as lower interest rates and lower inflation improve consumers’ purchasing power. However, the long period of weak confidence in the economy continues to weigh on consumption and investment.

Read more

Economic Outlook

The monetary policy tightening initiated by the ECB in 2022 halted economic growth in Finland and sent home prices tumbling. So why isn’t the monetary policy loosening that began a year ago having a positive effect on the Finnish economy yet?

Read more