- Name:

- Richard Hayes

- Title:

- Chief Strategist, Transaction Banking

Den här sidan finns tyvärr inte på svenska.

Stanna kvar på sidan | Gå till en relaterad sida på svenska4 min to read

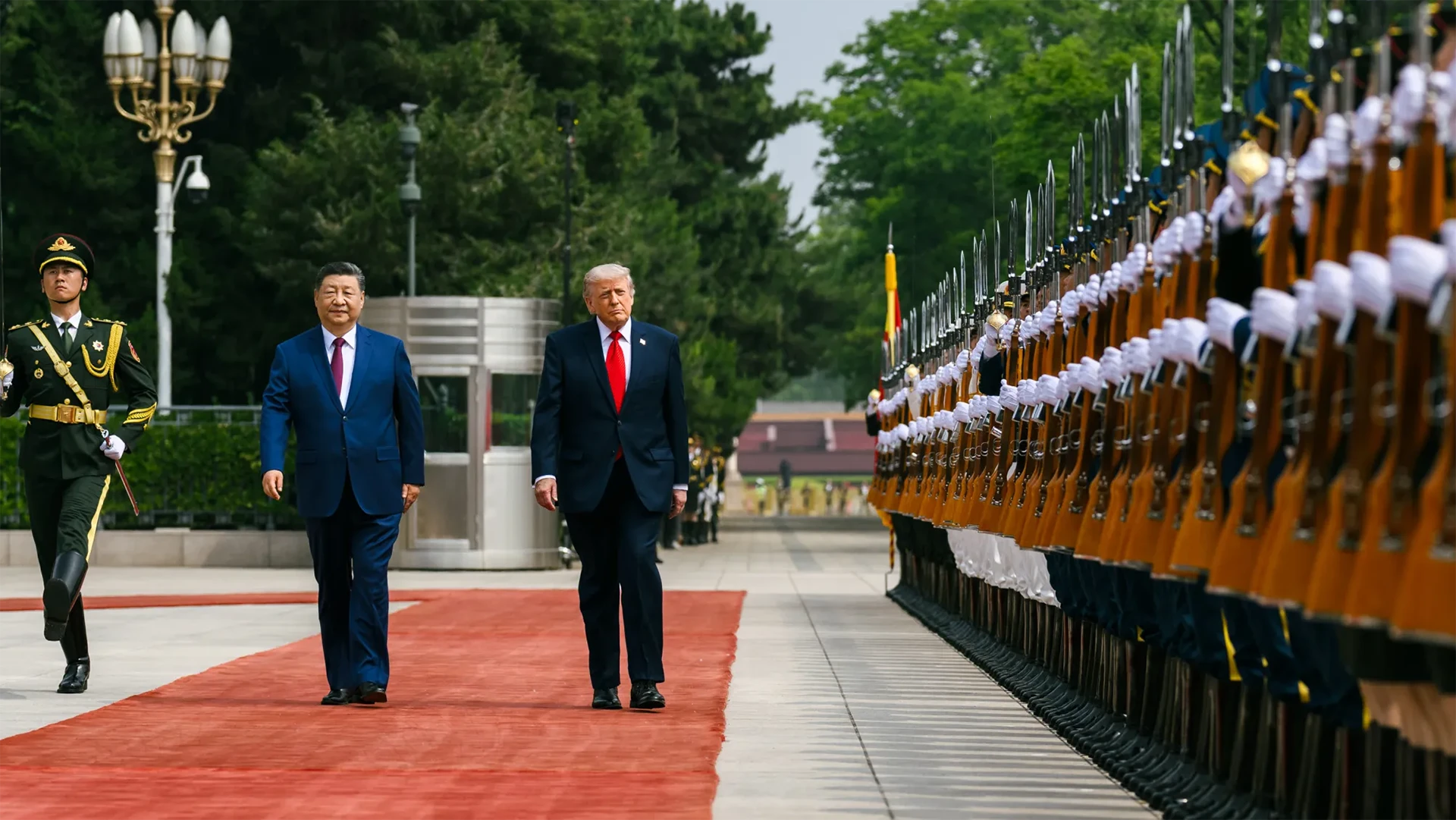

The recent Beijing summit won't reset US-China relations, but it offers something businesses have craved since 2018: predictability. We break down what "managed stability" means for Nordic companies navigating global supply chains.

The recent summit between President Xi and President Trump in Beijing marks a significant shift in the world's most scrutinised trade relationship. While the US-China dynamic may seem distant from Nordic operations, its ripple effects shape global trade policy, supply chains and capital flows in ways that directly impact European businesses.

The summit delivered symbolic gestures rather than breakthrough agreements. China committed to purchasing US agricultural products and signed deals for approximately 200 Boeing aircraft—both smaller than anticipated but commercially significant after years of stalled negotiations. Perhaps most importantly, both nations agreed to restart the US-China Board of Trade, creating a structural channel for resolving commercial disputes and reducing regulatory surprises.

However, what wasn't discussed is equally telling. There were no tariff reversals, no semiconductor technology concessions, no progress on industrial subsidies and no binding commitments on market access. This wasn't a relationship reset—it was an agreement to manage ongoing rivalry more predictably.

The summit introduced what experts are calling "managed stability"—a framework where Washington and Beijing accept their ongoing rivalry but establish guardrails to prevent shocks, miscalculations and economic escalation. This isn't broad cooperation but more an acceptance of controlled competition.

This approach offers businesses something they've desperately needed since 2018: breathing room. After years of perma-volatility, companies now have clearer signals about major policy moves, established mechanisms to prevent crises and selective cooperation in aligned sectors like energy and agriculture. Core competition will continue in semiconductors, AI, EVs, batteries, and rare earth minerals—but with more predictability.

This approach offers businesses something they've desperately needed since 2018: breathing room.

The impact varies dramatically by sector. Semiconductors and AI remain zero-sum battlegrounds with no change expected. Electric vehicles and battery technology face intensifying competition as supply chains regionalise, though critical minerals remain a necessary cooperation point.

Industrial machinery and automation represent managed stability at its best, with China signalling openness to foreign technologies while US firms maintain strong demand for Chinese products. Nordic machinery exporters stand to benefit from more predictable market access.

Consumer electronics will see continued supply chain diversification, but China remains the anchor for high-value components. The summit reduces sudden tariff shock risks, making "China-plus-one" strategies more viable—though working capital requirements remain significant.

For Nordic companies, this new landscape presents opportunities. The region's strong transatlantic ties combined with a non-threatening geopolitical profile offer strategic advantages that purely American or Asian competitors lack.

The key is understanding that while sudden tariff shocks should decrease, strategic competition continues. Companies need dual-track approaches: maintaining China relationships for certain activities while developing alternative manufacturing hubs for others. Supply chains are becoming more distributed, with China increasingly serving as the high-value manufacturing hub within broader regional networks spanning ASEAN, Mexico, and India.

Managed stability appears likely to persist for the next few years, offering better planning horizons and lower headline risk. However, businesses must remain prepared for alternative scenarios, including potential geopolitical or regulatory shocks that could trigger rapid disruption.

The US-China relationship may not be the world's largest by trade volume, but it remains the most important fault line in global trade policy. For Nordic businesses, understanding and adapting to this new era of managed competition isn't optional; it's essential for strategic planning in an increasingly complex global marketplace.

The Corporate Insights newsletter sums up the top business insights and ideas from Nordea experts and beyond. The newsletter is for business leaders and professionals, ambitious entrepreneurs and for anyone who is interested in the latest financial developments.

Read more

Sustainability

Companies that proactively engage with their Scope 3 emissions are finding opportunities to deliver business value beyond compliance, from more strategic procurement decisions to greater supply chain resilience.

Read more

Fraud

AI-driven scams are now seen as the most difficult type of fraud to guard against in the Nordic region, according to new findings from our latest Nordic Pulse survey.

Read more

Sustainability

Key reflections from a Sustainability Nordic Strategy Talk, where the lens was set on sustainability and procurement.

Read more