Watch the Economic Outlook webinar

Get the economic outlook for Finland directly from our economists in this on-demand webinar (in Finnish).

See the webinarDenne siden findes ikke på norsk

Bli værende på denne siden | Fortsett til en lignende side på norskThe Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

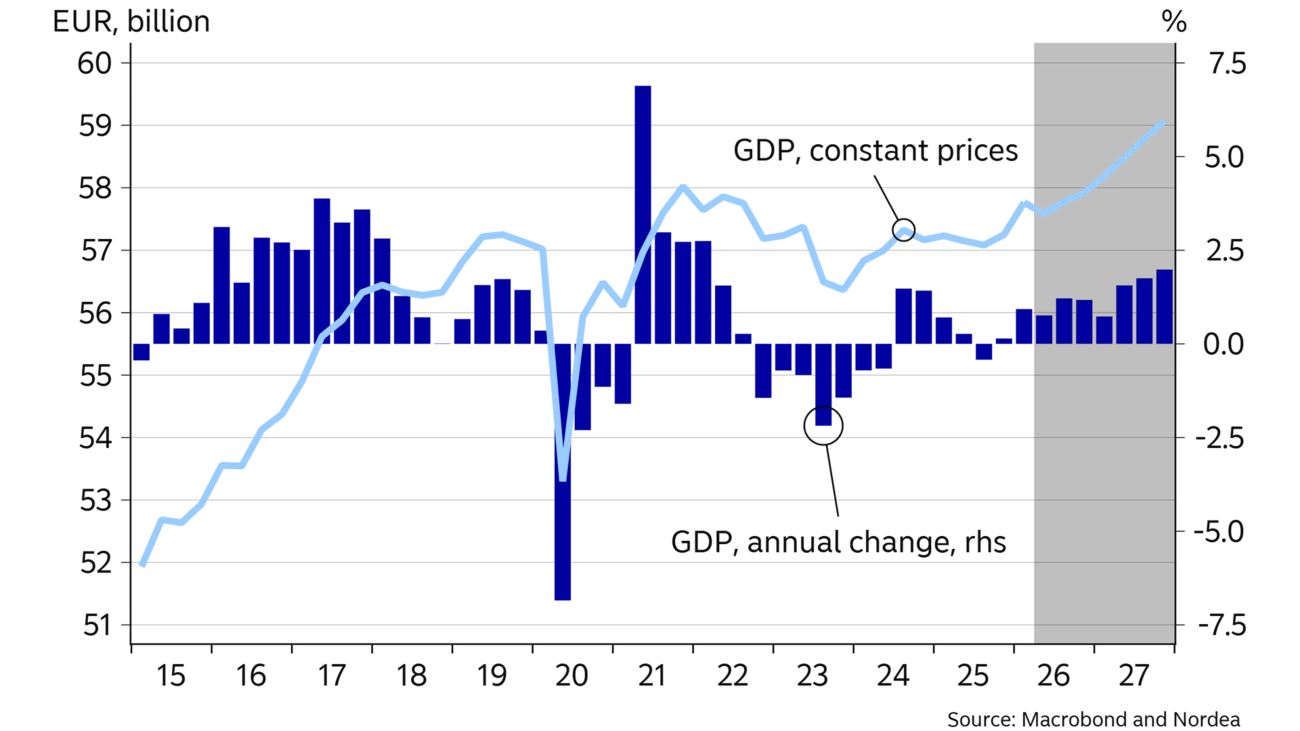

According to the data, Finland's GDP grew by 0.3% in the final quarter of last year and, based on preliminary figures, by as much as 0.9% in the first quarter of this year compared with the previous quarter. Growth has been broad-based, driven by private consumption, industry and investment.

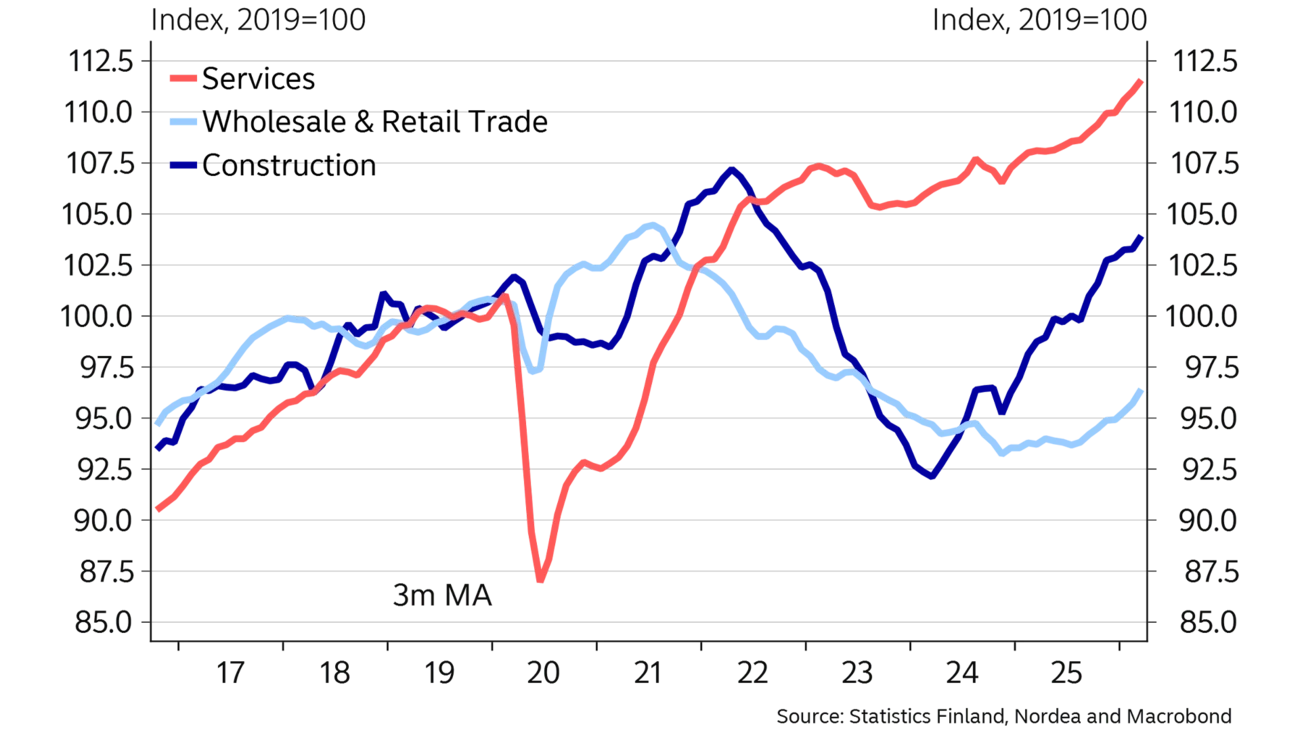

The recovery in consumption is visible in retail trade, which has turned upward after four years of decline. However, higher fuel prices following the war with Iran, together with rising interest rates, are likely to slow the recovery in purchasing power and have already weakened consumer confidence. Even so, card data for March and April suggest that private consumption has remained resilient despite the negative backdrop.

Data-centre projects and infrastructure construction are bringing the construction sector back to growth, even though residential construction is still expected to contract this year.

Orders and output in the export sector have picked up strongly since last autumn. In particular, orders have risen sharply in the machinery, shipbuilding and defence industries, pointing to growth in goods exports. Industrial employment has also started to recover, and unemployment across the economy is therefore expected to begin declining as growth gathers pace.

We expect Finland's GDP to grow by 1.0% this year and by 1.5% next year. The forecast balances the stronger-than-expected start to the year against the negative shocks stemming from the Middle East crisis. If conditions in the energy markets stabilise soon, growth over the forecast period could turn out clearly stronger than expected as the economy's positive momentum gathers force. On the other hand, a further escalation of the oil crisis and a more prolonged rise in fuel prices and interest rates could once again weaken purchasing power and significantly worsen the growth outlook.

Consumer price inflation in Finland was still close to zero at the start of the year, but high electricity prices early in the year and the rise in fuel prices following the Middle East conflict in March have clearly pushed inflation higher. Inflation is expected to average 1.4% this year, after domestic inflation remained at 0.3% last year. In addition to oil prices and their indirect effects, higher interest rates are beginning to feed through into domestic inflation. We expect the average interest rate on housing loans next year to be around one percentage point higher than at present. Core inflation is expected to pick up only moderately.

Last year, employees' real earnings rose by as much as 2.7%, returning to their 2021 level. This year, real earnings are still expected to increase, but growth will slow to around 1.5% as inflation accelerates.

| 24 | 25E | 26E | 27E | |

|---|---|---|---|---|

| Real GDP, % y/y | 0.4 | 0.2 | 1.0 | 1.5 |

| Consumer prices, % y/y | 1.6 | 0.3 | 1.4 | 1.8 |

| Unemployment rate, % | 8.4 | 9.7 | 10.3 | 9.1 |

| Wages, % y/y | 3.4 | 3.0 | 3.1 | 2.4 |

| Public sector surplus, % of GDP | -4.4 | -3.4 | -3.1 | -2.6 |

| Public sector debt, % of GDP | 82.4 | 88.5 | 90.0 | 91.1 |

| ECB deposit interest rate (at year-end) | 3.00 | 2.00 | 3.00 | 3.00 |

Real GDP

Output volume

The forecast balances the stronger-than-expected start to the year against the negative shocks stemming from the Middle East crisis.

The recovery in households' purchasing power has finally begun to feed through into private consumption. In March, both retail sales volumes and service output were up by nearly 4% year-on-year. Households have built up larger financial buffers in recent years, and so far private consumption does not appear to have reacted strongly to higher fuel prices and interest rates. Nordea's card data show that consumption also remained strong in April, despite faster inflation, higher interest rates and weaker consumer confidence. We expect private consumption to grow by around 1% this year and next. Public consumption, by contrast, is still expected to contract this year as a result of fiscal consolidation measures.

The rise in unemployment has levelled off, but the rate remains high at 10.4%. As the economy strengthens, the labour market is also expected to improve gradually. We expect the unemployment rate to fall to 8.5% by the end of 2027.

The housing market has remained subdued, and transaction volumes at the start of the year were lower than a year earlier. Rising interest rates and weaker consumer confidence are likely to keep the housing market muted this year as well.

Weak housing demand, excess supply in the rental market and a decline in state-subsidised affordable rental construction will keep residential construction weak this year and next.

At the same time, data-centre projects have boosted the construction sector. Over the past year, as much as 18% of the volume of building permits applied for has been related to data centres. In such projects, permits are typically sought for the entire complex at once, even though construction proceeds in phases. As a result, permit volumes may overstate the amount of construction in the near term. The government's increased support for renovation projects is also likely to boost renovation activity next year.

Investment is expected to grow by as much as 5.6% this year. In addition to data centres, public investment will increase this year due to fighter jet purchases and other defence spending.

The industrial outlook has also improved over the past year as order books have strengthened. In particular, shipbuilding, machinery and defence industries are seeing strong growth. The expanding order backlog is also expected to support export growth this year.

At the same time, higher oil prices and interest rates may slow economic activity in Europe and, in turn, weaken export demand. Exports therefore remain subject to downside risks.

Public sector deficits have narrowed in recent quarters. Consolidation measures have brought expenditure growth to a halt, while the improved cyclical backdrop has started to lift tax revenues. Public finances are expected to improve gradually this year and next. However, the recording of fighter jet purchases as public expenditure from this year onward, together with higher interest costs, will keep the deficit large even though the underlying balance is improving.

Further consolidation measures are therefore needed to curb the rise in public debt. The debt-to-GDP ratio is expected to exceed 90% this year.

Get the economic outlook for Finland directly from our economists in this on-demand webinar (in Finnish).

See the webinar

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more

Economic Outlook

The Middle East war and the closure of the Strait of Hormuz disrupt energy and supply chains and weaken confidence. We therefore downgrade our global growth forecast, while central banks face rising price pressures.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economic Outlook

The war in the Middle East challenges the resilience of international and Danish economies, but the foundation for continued growth is quite solid.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more