1.5%

Estimated growth in Mainland GDP in 2026

Sivua ei ole saatavilla suomeksi

Pysy sivulla | Siirry aiheeseen liittyvälle suomenkieliselle sivulleThe overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates. Registered unemployment will remain at a low level, but may edge up slightly. Inflation has been higher than expected and clearly above the inflation target for a long time. Higher oil and commodity prices further raise the inflation outlook. Norges Bank hiked the policy rate in May and will probably hike it one more time this year. The krone has strengthened and may strengthen a bit further, especially against the USD.

Growth in the Norwegian economy picked up last year to slightly above the economy’s trend growth. Registered unemployment has remained fairly stable at a low level over the past two years and has fallen somewhat so far this year. The purchasing power among households has increased substantially in the last two years and higher consumption has lifted growth in the Norwegian economy. Although prices have risen significantly in recent years, wages have increased more. Including this year, median wages have risen by 27% over the past five years. Therefore, a given level of debt has become correspondingly easier to carry, all else equal. Many underestimate these effects.

The outlook is slightly weaker than in previous forecasts, mainly because interest rates are edging up rather than down. Though purchasing power will increase less than in the two preceding years, it will increase. The main wage settlement for 2026 ended with a framework of 4.4%, the same as last year. And as last year, wage growth could end up slightly higher than this. With CPI inflation estimated at just above 3%, the outlook is for a continued solid increase in real wages. One or two rate hikes will dampen purchasing power growth but not eliminate it. We also expect real wages to increase next year.

The construction sector has struggled and there is no sign of a near-term upswing. Costs have risen sharply in recent years and many developers have been waiting for lower interest rates and higher existing-home prices to narrow the gap to prices of new homes. With interest rates moving higher again, that process has been put on hold. Therefore, sales of new homes are unlikely to increase much over the next couple of years.

On the other hand, higher oil prices could mean that oil investments do not fall as much as previously assumed. Other parts of the export sector also benefit from higher commodity prices. Nor do we see any signs that the increase in oil-funded spending in the government budget will be scaled back going forward. Lower duties on petrol and diesel have resulted in lower prices than before the war in Iran. So far, households and businesses have not only been shielded from the direct effects of higher oil prices, they have received a small stimulus. Even if growth abroad is likely to be somewhat weaker, there are several factors at home that contribute positively to growth. Overall, and taking the tax cuts into account, the marginal effects of higher oil prices are probably small for the Norwegian economy.

Therefore, we envisage only slightly weaker growth in the Norwegian economy than last year, close to—or somewhat below—trend growth of 1½–1¾%. Registered unemployment has fallen from 2.2% in November to close to 2.0% now. With slightly weaker growth ahead, we believe registered unemployment could gradually rise by one or two tenths again.

| 24 | 25 | 26E | 27E | |

|---|---|---|---|---|

| Real GDP (mainland), % y/y | 0,6 | 1,8 | 1,5 | 1,3 |

| Household consumption | 1,5 | 2,8 | 2,0 | 1,8 |

| Core inflation (CPI-ATE), % y/y | 3,7 | 3,1 | 3,2 | 2,7 |

| Annual wage growth | 5,6 | 4,9 | 4,6 | 4,0 |

| Unemployment rate (registered), % | 2,0 | 2,1 | 2,1 | 2,2 |

| Monetary policy rate (end of period) | 4,5 | 4,0 | 4,5 | 4,5 |

| EUR/NOK (end of period) | 11,8 | 11,8 | 10,75 | 10,75 |

1.5%

Estimated growth in Mainland GDP in 2026

2.2%

Estimate of registered unemployment at the end of 2027

4.5%

Estimate of the key policy rate at the end of 2027

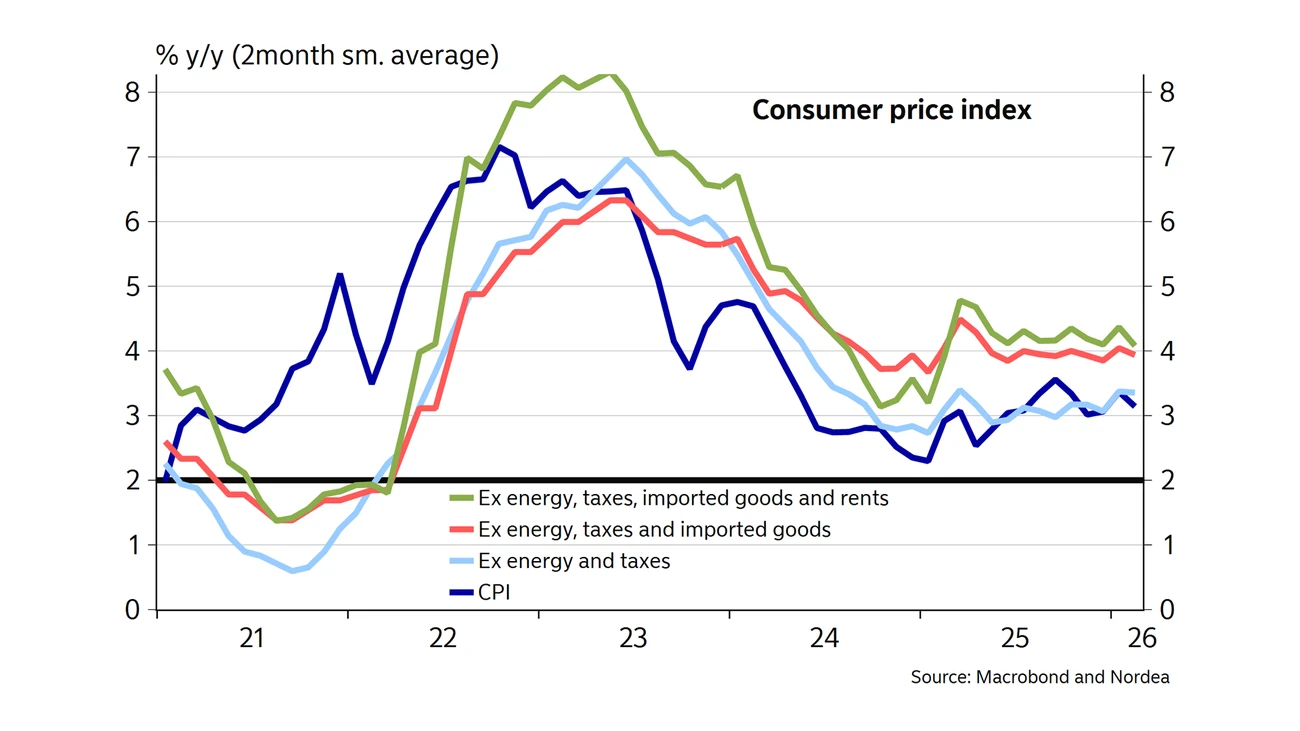

Higher oil and gas prices were an important reason why CPI inflation rose in 2022. Over time, this spilled over into price growth for other goods and services. However, over the past couple of years, inflation both with and without energy prices have been broadly similar, around 3%. Therefore, it is not energy prices that are keeping inflation high now. If anything, CPI inflation adjusted for energy prices has trended slightly higher recently. Adjusted for prices on imported goods, inflation has held at around 4%. Additionally, if we also remove rents, inflation in the remainder has been a bit higher.

Therefore, it is Inflation in domestically produced goods and services that is now high and is contributing to inflation remaining well above the 2% inflation target. It is natural to view this in connection with the strong wage growth we have seen in recent years. Tax reductions on petrol and diesel dampen the impact of the Middle East conflict on headline inflation, but we will see indirect effects through higher prices for transport, imported goods and intermediate inputs. With wage growth still high, there is little prospect that inflation will fall markedly in the near term.

The krone has strengthened broadly so far this year and Norges Bank’s turnaround has contributed to this. The rise in oil and gas prices has also meant that oil companies have bought more kroner to pay taxes to the state. In addition, Norges Bank has shifted from being a net seller of kroner last year to becoming a significant net buyer at the start of the year.

Even if oil prices were to fall somewhat going forward, we still expect a moderately stronger krone ahead. Apart from higher interest rates, increased focus on energy security may lead to higher investment in oil- and gas-related assets and thus more capital inflows to Norway. Second, we expect a markedly weaker dollar over the next two years, which historically has helped smaller currencies such as the krone strengthen against the major ones.

The two rate cuts from Norges Bank last year were based on an expectation that inflation would continue to ease. That did not happen and underlying inflation has been clearly higher than projected. In addition, growth in the Norwegian economy has picked up and unemployment has fallen somewhat again.

The Middle East conflict comes on top of this and implies that inflation could rise further. A stronger krone does help — both directly because imported inflation becomes lower than otherwise, and indirectly through weaker profitability in the export industry resulting in a lower wage-setting capacity. However, Norges Bank cannot take the krone’s strength for granted, as part of it is attributable to expectations of higher interest rates.

We think Norges Bank means business and will hike again this autumn

Norges Bank is focused on preserving confidence in the inflation target. The bank is concerned that high inflation over a long period could cause firms and employees to start planning for inflation to remain high. To ensure that inflation returns to the 2% inflation target within a reasonable time, Norges Bank has turned around and raised the policy rate again.

We think Norges Bank means business and will hike the rate again this autumn. This contribute to our view of a slightly stronger krone, which will be an important factor bringing inflation down. However, price and wage inflation must fall a great deal before Norges Bank starts thinking about rate cuts again. We do not think that will happen over the next two years.

Get the economic outlook for Norway directly from our economists in this on-demand webinar (in Norwegian).

See the webinar

Economic Outlook

The Middle East war and the closure of the Strait of Hormuz disrupt energy and supply chains and weaken confidence. We therefore downgrade our global growth forecast, while central banks face rising price pressures.

Read more

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economic Outlook

The war in the Middle East challenges the resilience of international and Danish economies, but the foundation for continued growth is quite solid.

Read more

Economic Outlook

The Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

Read more

Economic Outlook

Sweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

Read more