Watch the Economic Outlook webinar

Get the economic outlook for Sweden directly from our economists in this on-demand webinar (in Swedish).

See the webinarSiden findes desværre ikke på dansk

Bliv på siden | Fortsæt til en relateret side på danskSweden is on a solid footing and can withstand several of the challenges arising from the war in the Middle East. A favourable circumstance is the low inflation rate this year. Uncertainty is high. A key factor will be how long the Strait of Hormuz remains closed.

We are living in turbulent times. The war in Iran is creating uncertainty and clouding the outlook. The longer the conflict in the Middle East continues, the greater the economic effects will be. This puts pressure on political leaders around the world to find a solution to end the conflict.

We assume that the Strait of Hormuz will reopen by the summer and that the economic consequences will therefore remain limited. However, some damage has already been done. Delayed effects of higher energy prices and the shortage of fertilizer for spring sowing will probably lift inflation in many parts of the world.

The risk is that the Strait of Hormuz will remain closed and that companies’ higher pricing plans result in larger price increases. In that case, it would likely lead both the ECB and the Riksbank to raise policy interest rates. A more prolonged conflict would be felt by the Swedish economy, but the situation would have to worsen significantly before it will lead to more severe economic consequences.

The Swedish economy is fundamentally robust. The business sector is competitive, wage formation is well-ordered, employment is high, and public finances are sound. Households are interest-rate-sensitive, but less so than before the pandemic. In our baseline scenario, interest rates rise only gradually over the forecast period. This means the conditions are in place for solid growth in the Swedish economy.

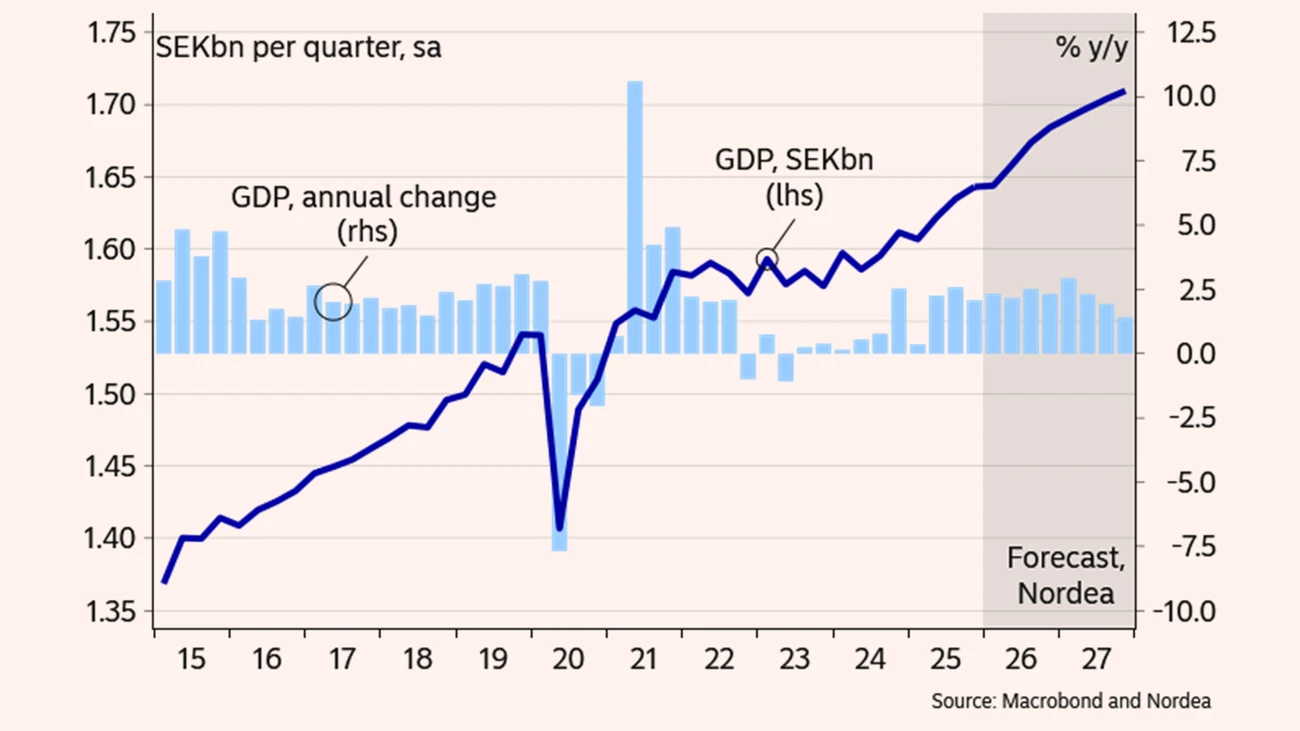

The economic spillovers from the war in the Middle East are also reaching Sweden. The impact occurs primarily through global demand, inflation and interest rates, as well as through the risk of deteriorating sentiment. GDP growth slows, but the effects are moderate in the baseline scenario.

The dip in GDP growth that appears to have occurred at the beginning of the year is assessed to be temporary. Growth rebounds in the second quarter and the economy expands at a solid pace in 2026. Unemployment declines, spare capacity in the economy is absorbed, and the business cycle normalises next year. With higher resource utilisation, the wheels turn faster and the GDP-growth rate slows slightly in 2027.

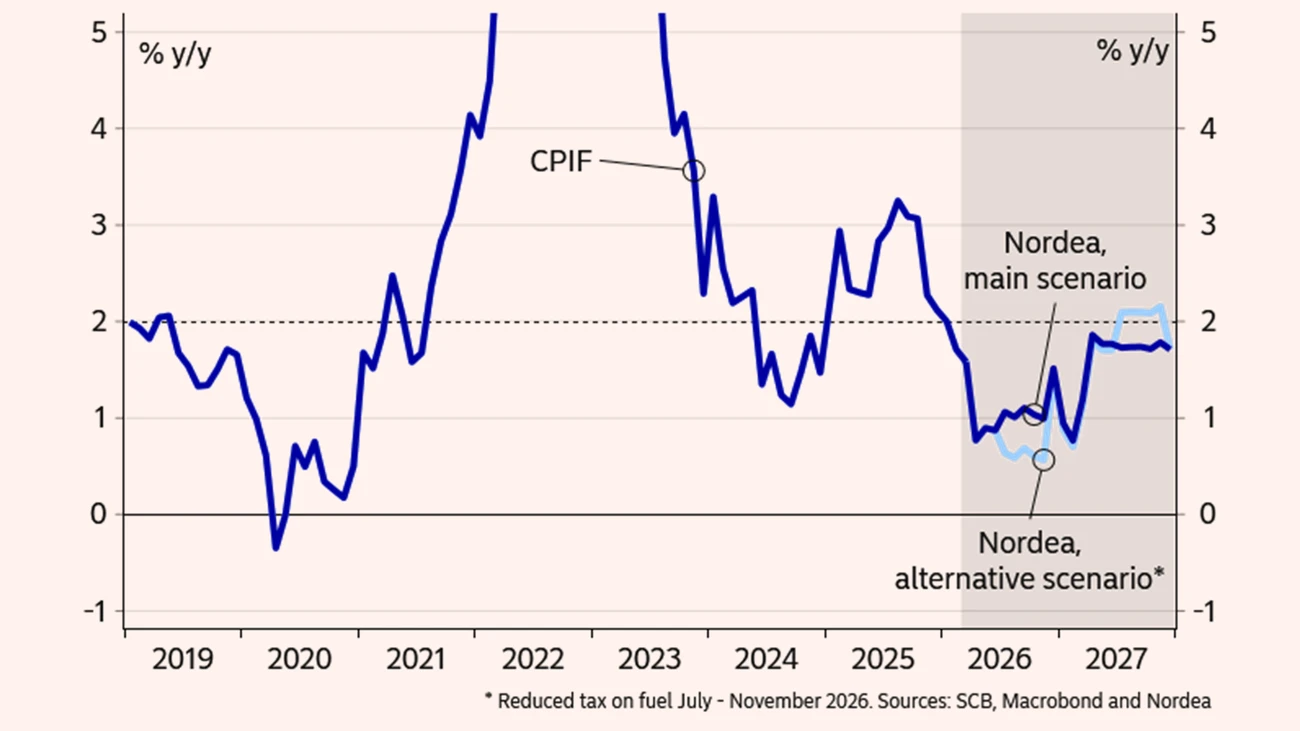

Inflation is at its lowest in the near term and then rises gradually from an unusually low starting level. In the baseline scenario, the inflation target is not threatened and the Riksbank leaves the policy rate unchanged this year. A normalisation of the business cycle and inflation close to the 2 percent target justify a somewhat higher policy rate in 2027. Our forecast is a policy rate of 2.25 percent at the end of 2027.[1]

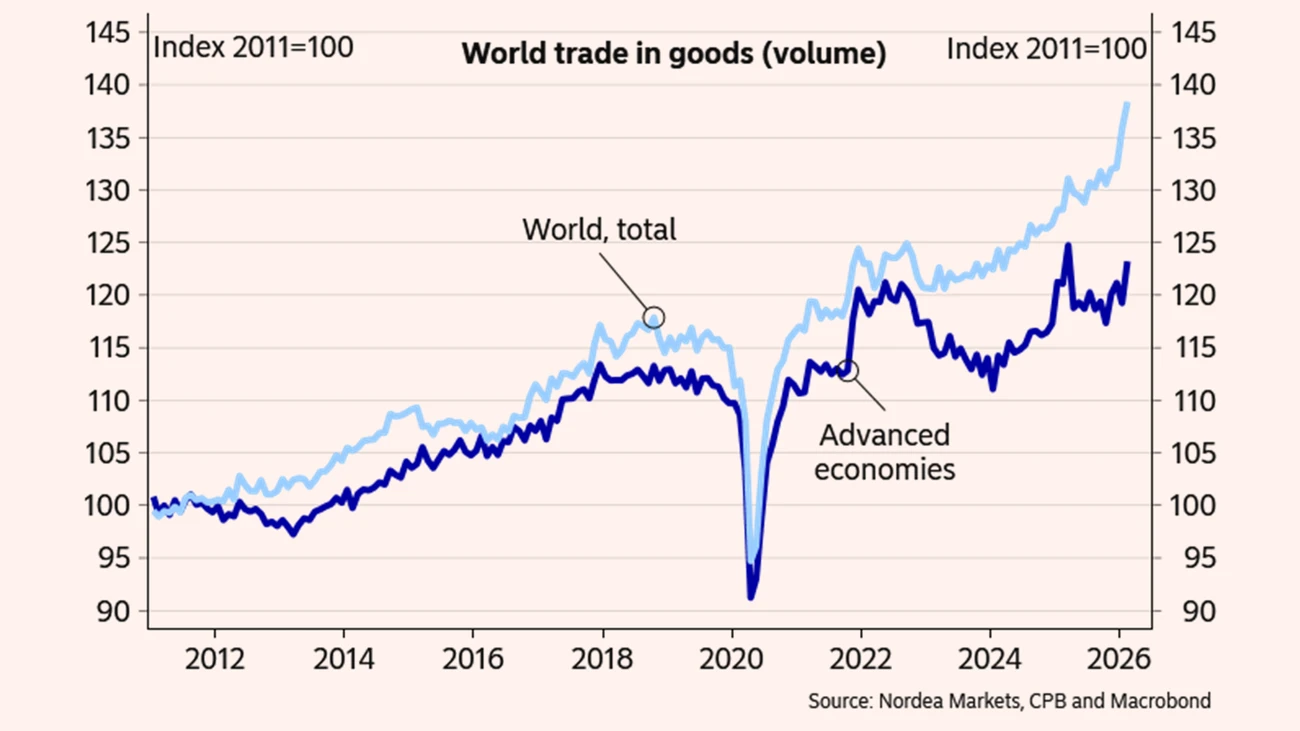

Exports are unexpectedly strong. Total exports increased by almost 4 percent last year, despite the shift in US trade policy and despite goods exports across the Atlantic declining by 9 percent. As in recent years, exports of services posted the highest growth, at 5.2 percent, but goods exports also recorded a solid increase of 3.3 percent.[2]

In the first quarter of this year, exports of goods appear to have been at a decent level. In addition, order intake is rising according to indicators such as the National Institute of Economic Research Tendency Survey and the PMI, which points to export growth in the first half of this year. The upturn at the beginning of the year coincides with a sharp rise in world trade.

There may be temporary factors behind the unexpectedly strong upturn in international demand at the beginning of the year. A Supreme Court ruling in the US in February, which lowered tariffs for certain regions, may have led to orders and deliveries being brought forward globally. Nor can it be ruled out that the war in the Middle East has caused orders to be placed earlier, also boosting orders to Swedish manufacturers. At the same time, the potential for global demand is significant, not least on the back of the trade agreements the EU has recently concluded with several countries and regions. Sweden’s defence industry is also expected to contribute to higher exports.

After a strong increase around mid-year, export growth levels off. Measured as an annual average, the increase is close to the growth rates we saw last year. The composition is also similar, with a continued strong trend in the increasingly important export of services. In other words, the conflict in the Middle East is assessed to have only limited effects on Swedish exports.

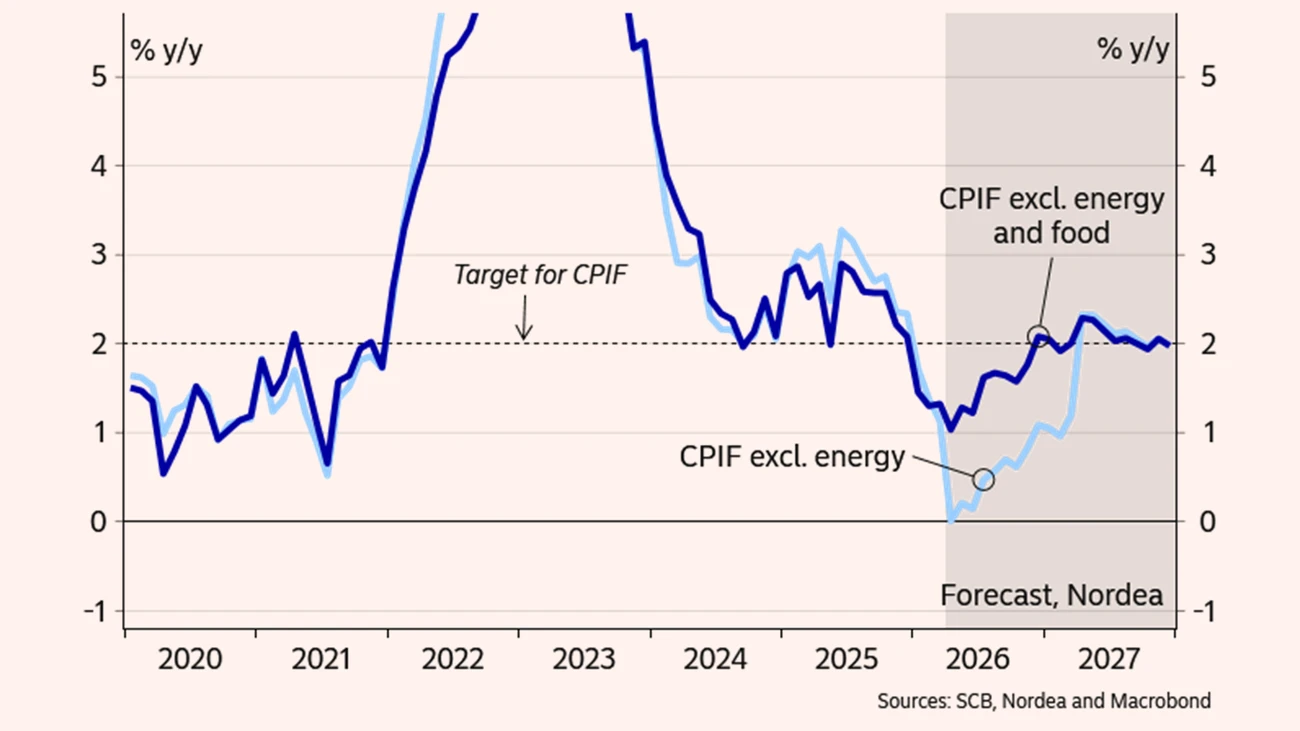

A favourable circumstance for Sweden is that inflationary pressure is low at the outset. The multi-year strengthening of the trade-weighted exchange rate (KIX) is pulling down inflation substantially. The decline in energy prices in recent years has also reduced firms’ costs and, ultimately, the need to raise consumer prices. In addition, VAT on food was halved in April and the tax on fuels was cut in May.

Further, tax on fuel could be cut further, especially if the oil price rises further from today’s level. The EU has given the green light to a further reduction of SEK 3 per litre. If implemented, it would help lower CPIF inflation by an additional 0.4 percentage points over the period it applies. In our baseline scenario, we do not assume an additional fuel-tax cut, but the chart below shows an alternative scenario for the CPIF path with a full tax reduction. At the same time, electricity prices are expected to be close to normal and mainly vary with the season, in line with pricing in the electricity futures market.

Fiscal policy therefore has a significant impact on the inflation path, even if the fuel tax is not reduced further. Overall, the Riksbank has room to wait. Since the Strait of Hormuz is assumed to reopen this summer and the supply of oil and other commodities is assumed to improve, the baseline scenario is that the inflation impulses fade and the Riksbank keeps the policy rate unchanged at today’s level throughout 2026.

At the end of 2026 and at the beginning of next year, underlying inflation is expected to rise, among other things as the price-dampening effects of the earlier appreciation of the krona fade and certain delayed effects of currently high oil and commodity prices feed through to consumers. Inflation will not become uncomfortably high, but together with higher resource utilisation it justifies two rate hikes and a normalisation of the policy rate to 2.25 percent next year, from the current level of 1.75 percent.

The baseline scenario is therefore that inflation is low this year and close to the inflation target next year. This means household purchasing power develops well thanks to rising employment, higher wages, and lower taxes. In real terms, household income increases by just over 3 percent in 2026 and by just over 2 percent in 2027. The dip in consumption that appears to have characterised the start of 2026 is, in our view, temporary and consumption increases at a solid pace going forward. At the same time, saving remains high over the forecast period.

Moderate inflation is the most important factor for households. Concern linked to the situation in the Middle East could make households hesitate to consume and to purchase housing, but we assess the effects to be small and, in any case, temporary. House prices rise in line with nominal incomes over the forecast period, i.e. by around 4.5 percent per year.

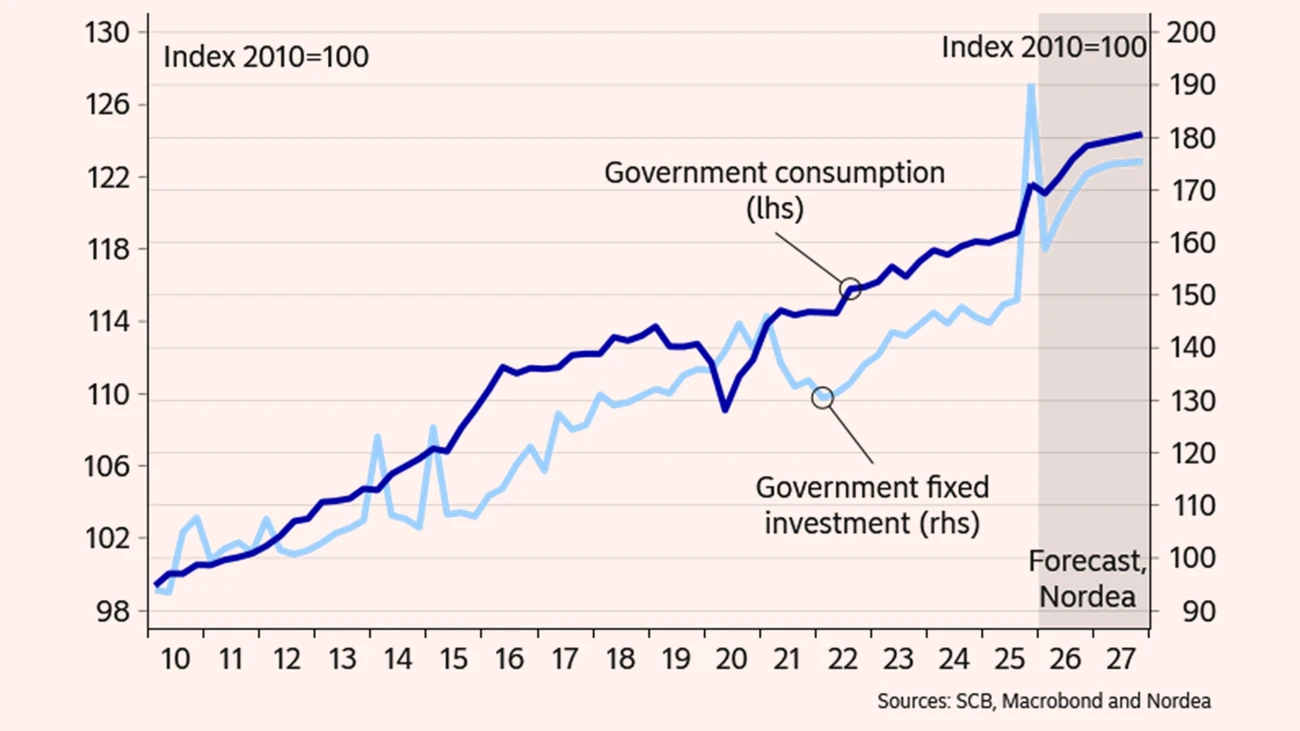

The build-up of defence contributes to raising GDP growth. This is reflected, among other things, in higher public consumption and growing public investment. There are exceptionally large swings between quarters. The effect on GDP is still gradual, however, as the fluctuations are often offset by countervailing items in imports, inventories, and fixed investment in other parts of the economy. Defence appropriations increase by almost 0.5 percent of GDP per year over the forecast period, which provides an indication of the effects over time.

Business investment is also growing. It has increased continuously since the pandemic, excluding housing. In particular, the development has been strong in the private service sector, and the sector has therefore managed much of the inflation and interest-rate shock that hit the economy especially in 2023. After slightly lower investment growth in 2025, it is expected to strengthen again starting this year. Housing construction remains subdued as population growth has almost completely come to a halt.

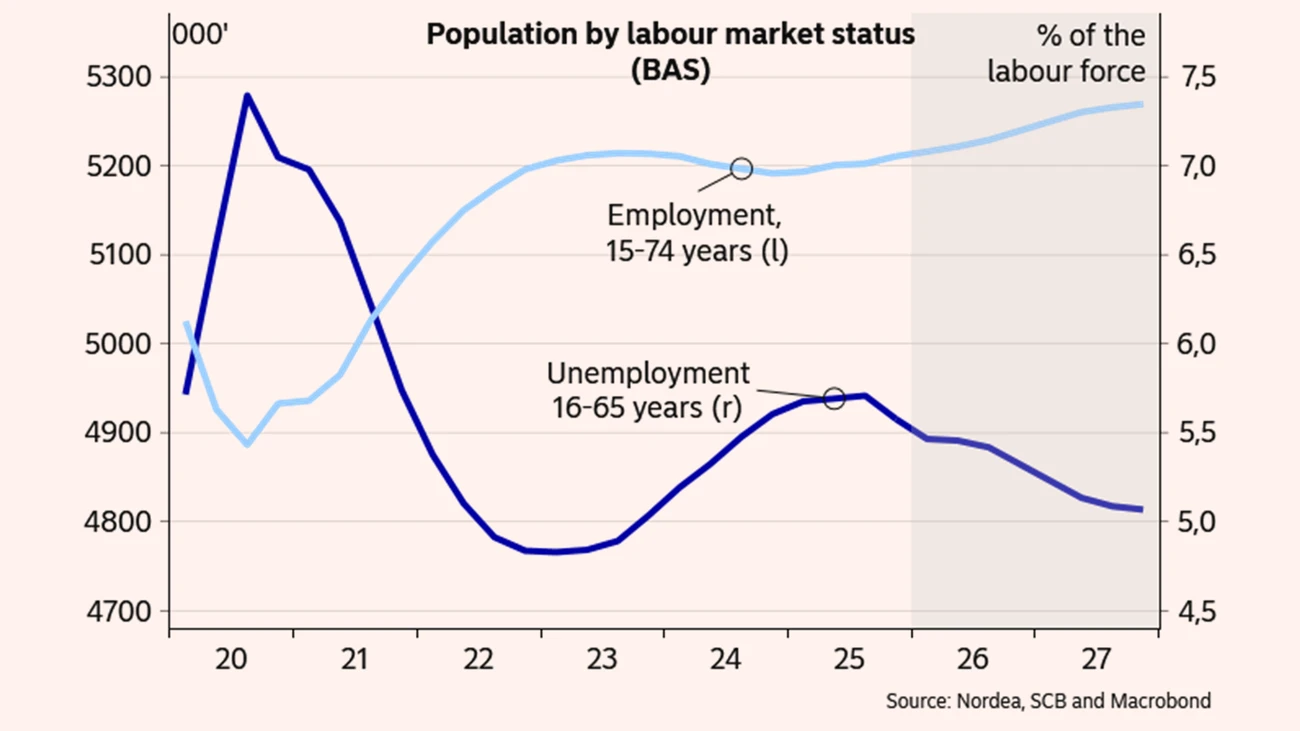

The labour market situation has improved over the past six months. The employment rate, i.e. employed persons relative to the population, has risen quickly and is close to the previous peak levels from 2022 and 2023. At the same time, labour supply is increasing and unemployment therefore declines slowly.

Forward-looking indicators point to continued growth in labour demand, albeit at a lower rate than over the past six months. For example, firms’ hiring plans have eased somewhat at the start of the year, while labour shortages remain below normal. New vacancies have bottomed out but are moving sideways rather than upward, while redundancy notices are close to a historical average.

Employment growth therefore eases in the near term, reflecting the soft patch in GDP growth at the beginning of the year. Employment still increases by around 1 percent both this year and next year. Unemployment according to Statistics Sweden’s Labour market status of the population (BAS) is currently 5.5 percent and declines slowly towards 5.0 percent at the end of next year. Unemployment is higher, according to the Labour Force Survey. It peaked at the end of last year at 9.0 percent and is expected to fall to around 7.5 percent at the end of 2027.

Today, unemployment is higher than normal, but the expected decline means that resource utilisation in the economy normalises next year, without becoming either strained or inflationary.

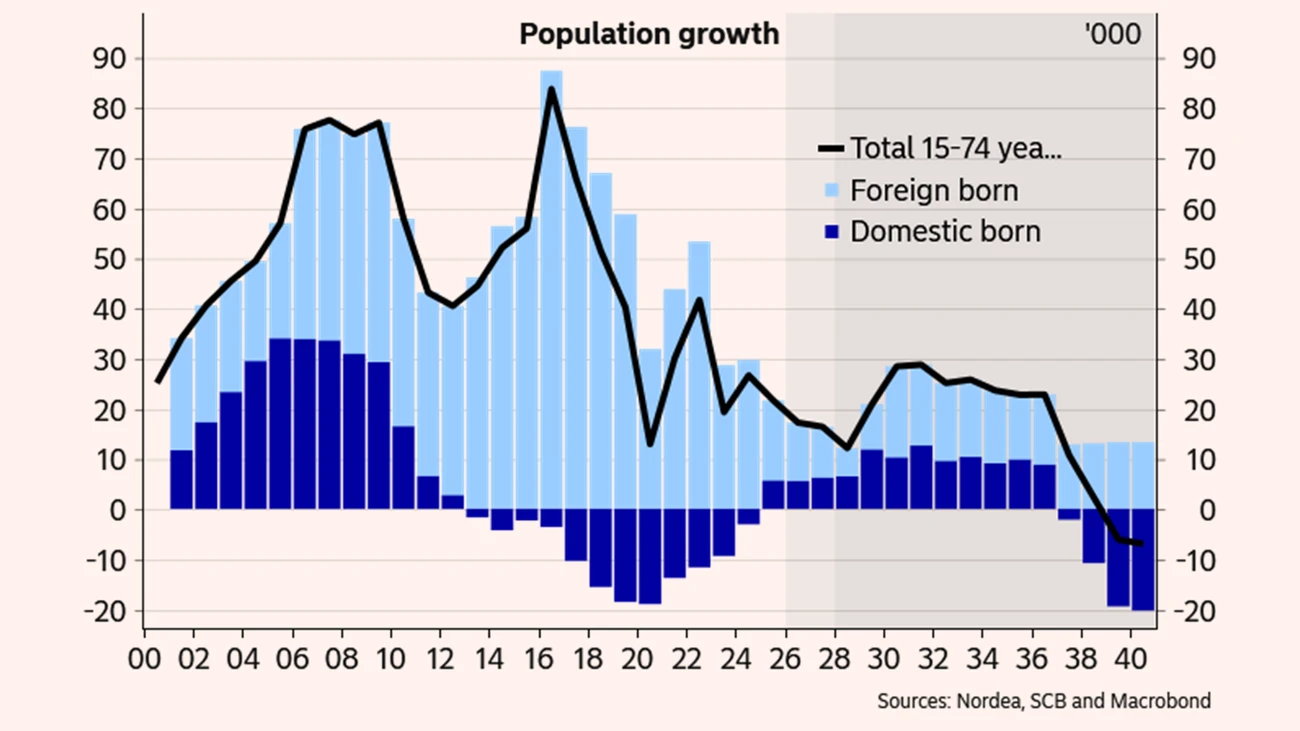

It is worth recalling that potential GDP growth has declined in recent years. The reason is that population growth has slowed markedly due to lower birth rates and lower immigration. Up to 2030, the population increases by an average of 0.2 percent per year, compared with about 1 percent per year during the 2010s.

As has been emphasised earlier, developments in and the consequences of the war in the Middle East are difficult to assess. If the Strait of Hormuz remains blocked longer than assumed, and inflation impulses becomes larger, the Riksbank could raises rates several times this year. This will in turn mean that growth would slow and the decline in unemployment would be interrupted. In such a scenario, Sweden could still grow faster than, for example, the euro area, but the growth advantage would narrow. That, combined with a more turbulent global environment, could weigh on the krona exchange rate. Given the events of the past year, one should be prepared for other storm clouds to flare up, even if the conflict in the Middle East subsides.

There are also possibilities for a stronger development. Swedish households’ financial position has improved markedly in recent years, which could result in a stronger increase in consumption than forecast. In addition, fiscal policy is expansionary. In that case, unemployment could fall faster and the Riksbank could tighten monetary policy earlier and more than assumed in this forecast.

| 2024 (SEKbn) | 2025 | 2026E | 2027E | |

|---|---|---|---|---|

| Private consumption | 2 894 | 1.6 | 2.5 | 2.8 |

| Government consumption | 1 698 | 0.7 | 3.0 | 1.7 |

| Fixed investment | 1 604 | 2.0 | 3.6 | 3.1 |

| - Industrial investment | 286 | -3.5 | 1.5 | 1.6 |

| - Residential investment | 194 | 0.1 | 3.9 | 2.3 |

| Stockbuilding* | 1 | 0.2 | 0.0 | 0.0 |

| Exports | 3 483 | 3.9 | 3.3 | 3.8 |

| Imports | 3 290 | 4.3 | 3.8 | 4.1 |

| Real GDP. % y/y | 1.5 | 2.6 | 2.4 | |

| Real GDP (calendar adjusted). % y/y | 1.8 | 2.3 | 2.1 | |

| Nominal GDP (SEKbn) | 6 392 | 6 570 | 6 808 | 7 087 |

| Unemployment rate (LFS). % | 8.8 | 8.5 | 7.9 | |

| Unemployment rate (BAS), % | 5.7 | 5.4 | 5.1 | |

| Employment (LFS). % y/y | 0.4 | 0.9 | 0.9 | |

| Consumer prices. % y/y | 0.7 | 0.5 | 1.9 | |

| Underlying prices (CPIF). % y/y | 2.6 | 1.2 | 1.6 | |

| Hourly earnings (NMO). % y/y | 3.7 | 3.4 | 3.3 | |

| Current account balance (SEKbn) | 340 | 287 | 267 | |

| Current account balance. % of GDP | 5.2 | 4.2 | 3.8 | |

| Trade balance. % of GDP | 4.0 | 3.1 | 3.1 | |

| General gov. budget balance (SEKbn) | -85 | -178 | -158 | |

| General gov. budget balance. % of GDP | -1.3 | -2.6 | -2.2 | |

| General gov. gross debt. % of GDP | 35.1 | 36.8 | 37.8 | |

| Monetary policy rate (end of period) | 1.75 | 1.75 | 2.25 | |

| USD/SEK (end of period) | 9.23 | 8.40 | 8.13 | |

| EUR/SEK (end of period) | 10.83 | 10.50 | 10.40 |

Get the economic outlook for Sweden directly from our economists in this on-demand webinar (in Swedish).

See the webinar

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economic Outlook

The war in the Middle East challenges the resilience of international and Danish economies, but the foundation for continued growth is quite solid.

Read more

Economic Outlook

The overall impact of the Middle East conflict on activity in the Norwegian economy is likely to be limited. Even so, the outlook is somewhat weaker than in previous forecasts because of higher, not lower, interest rates.

Read more

Economic Outlook

The Finnish economy has finally returned to broad-based growth, with both private consumption and industrial output picking up. Growth is also beginning to support the labour market and public finances. However, higher energy prices and rising interest rates in the wake of the Middle East crisis are expected to weigh on economic activity later in the year.

Read more