- Name:

- Helge Pedersen

- Title:

- Group Chief Economist

Den här sidan finns tyvärr inte på svenska.

Stanna kvar på sidan | Gå till en relaterad sida på svenskaHelge J Pedersen , Tuuli Koivu , Kjetil Olsen , Torbjörn Isaksson , Juho Kostiainen

Oil prices have surged from USD 60 to nearly USD 120 per barrel amid Middle East tensions, but the Nordic economies are expected to remain resilient. Our analysis shows the economic impact should be manageable if prices stabilise around current forward market expectations.

The ongoing war in the Middle East has triggered substantial energy price increases and financial market volatility. This analysis examines the potential growth and inflation implications for global and Nordic economies, with the ultimate impact depending on the war's duration and scale.

Oil prices rose from around USD 60 per barrel at the beginning of the year to over USD 70 before the war began in late February. Initially, price movements remained moderate, but after President Trump discussed deploying special ground troops and Iran announced the closure of the Strait of Hormuz (through which 20% of global oil production flows), prices spiked to nearly USD 120 per barrel on 9 March. However, prices fell to just over USD 90 the following day after G7 countries announced potential use of strategic oil reserves and Trump's statements about the campaign proceeding as planned.

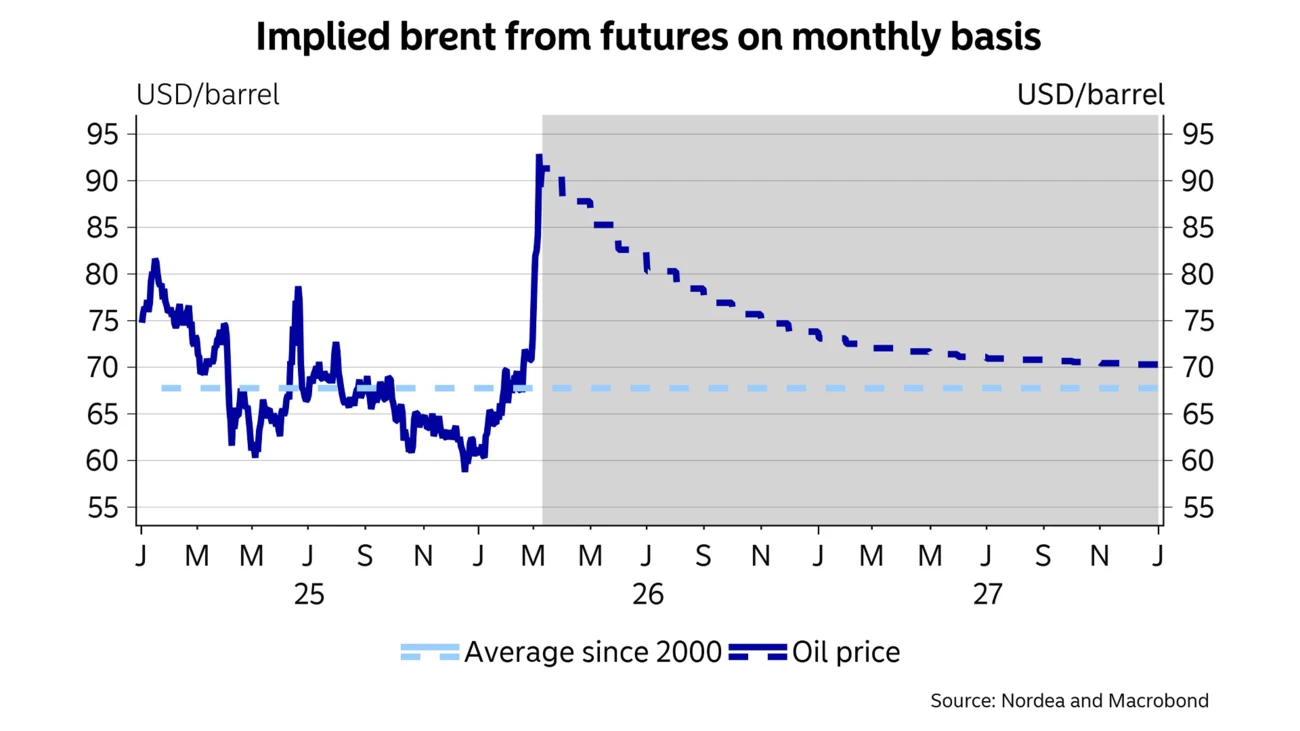

If oil prices stabilise around USD 90 per barrel, as suggested by forward prices peaking at USD 92 in spring before flattening to USD 75 by year-end, the global economic effects should remain limited. This represents approximately a 20% increase in oil prices compared to 2025 levels.

If oil prices stabilise around USD 90 per barrel, as suggested by forward prices peaking at USD 92 in spring before flattening to USD 75 by year-end, the global economic effects should remain limited.

Based on OECD multipliers, this would increase global inflation by up to 0.5 percentage points and reduce growth by around 0.2 percentage points over one year. For the eurozone, the ECB estimates a 20% oil price increase could raise inflation by 0.2-0.4 percentage points while reducing GDP growth by approximately 0.4 percentage points. However, the euro's 10% strengthening against the dollar over the past year should moderate these effects.

Denmark: With negligible trade ties to Iran and limited regional exposure (around 1% of total trade), Denmark's main vulnerability lies in energy dependency—35% of energy consumption stems from oil and 8% from natural gas. A permanent 20% oil price increase could reduce GDP by 0.2 percentage points and raise consumer prices by 0.4 percentage points. However, expected 3% wage growth in 2026, reduced electricity taxes, income tax cuts and food allowances for vulnerable populations should help maintain purchasing power despite energy price increases.

Finland: The impact will primarily affect household purchasing power through higher energy costs. Finland's reduced fossil fuel dependency (18.5% of energy consumption stemming from oil, 3.5% from gas in 2024) and minimal fossil fuel electricity generation provide some insulation from price shocks.

Norway: The war will increase inflation but have minimal negative growth effects. Government electricity subsidies shield households from higher European gas prices, while higher oil and gas prices will stimulate petroleum company investments. The negative effects are largely only indirect through lower growth abroad. But in an economy where the export sector is heavily commodity-based, the negative effect is expected to be small.

Sweden: Energy price increases could lift CPIF inflation by around 0.5 percentage points directly, with similar indirect effects over time. However, income growth is still healthy on the back of pay rises and tax cuts, and conditions remain in place for a continued recovery in domestic demand. The Riksbank is expected to maintain rates at 1.75% throughout 2026.

If oil prices develop as futures markets expect, the economic impact should be manageable for most countries. The Nordic economies appear well-positioned to weather this crisis due to strong fiscal positions, government support measures and diversified energy portfolios, although significant uncertainty remains about the war's duration and ultimate economic consequences.

Stay ahead of the curve with our expert economic insights and forecasts. Get the latest analysis on global and Nordic markets delivered straight to your inbox.

Read more

Economy

The Nordic region stands out for its economic resilience, innovation capacity and stable financial system – factors that continue to attract capital and support long term-growth.

Read more

Corporate insights

The landmark EU-Mercosur deal eliminates 91% of tariff lines for EU exports, creating major opportunities for Nordic companies while requiring careful risk management.

Read more

Economy

NATO’s new defense spending target will more than double European military budgets by 2035, with significant economic implications, clients heard at a recent Nordea event on Arctic security policy.

Read more