- Name:

- Marco Kisic

- Title:

- Head of ESG Research, Nordea Equities

Den här sidan finns tyvärr inte på svenska.

Stanna kvar på sidan | Gå till en relaterad sida på svenskaMarco Kisic

Amid geopolitical tensions and fractured global cooperation, Nordic companies are not retreating from their climate ambitions. Our Equities ESG Research team’s annual review shows stronger commitments and measurable progress on emissions reductions.

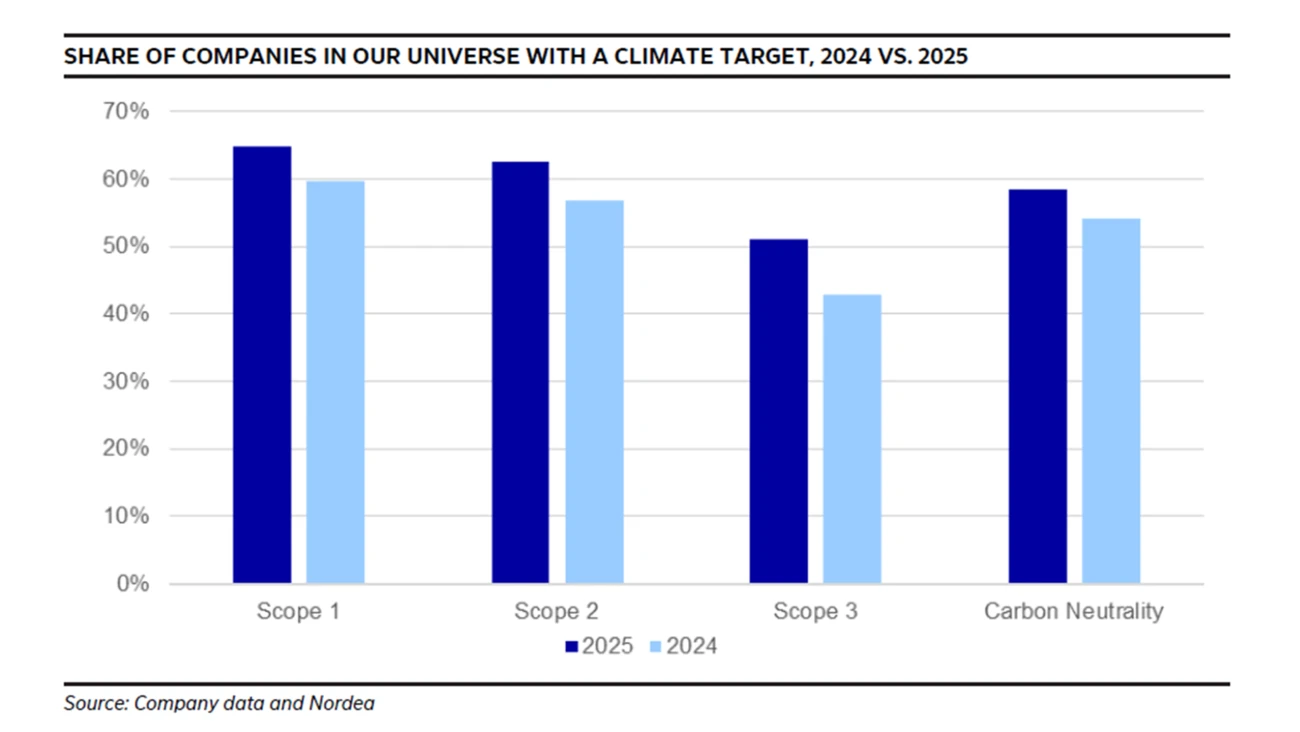

In today’s era of broken multilateralism, the question often arises: Are Nordic companies scaling back their climate ambitions? Our analysis of roughly 330 companies across the region shows the opposite. The decarbonisation rate targeted by our Nordic universe has edged up compared to last year, with more companies setting Scope 1 targets (64% versus 60%) and steeper medium-term reductions. The average target year for carbon neutrality is broadly unchanged at 2042.

All in all, our universe remains firmly committed to the transition, in our assessment.

All in all, our universe remains firmly committed to the transition, in our assessment.

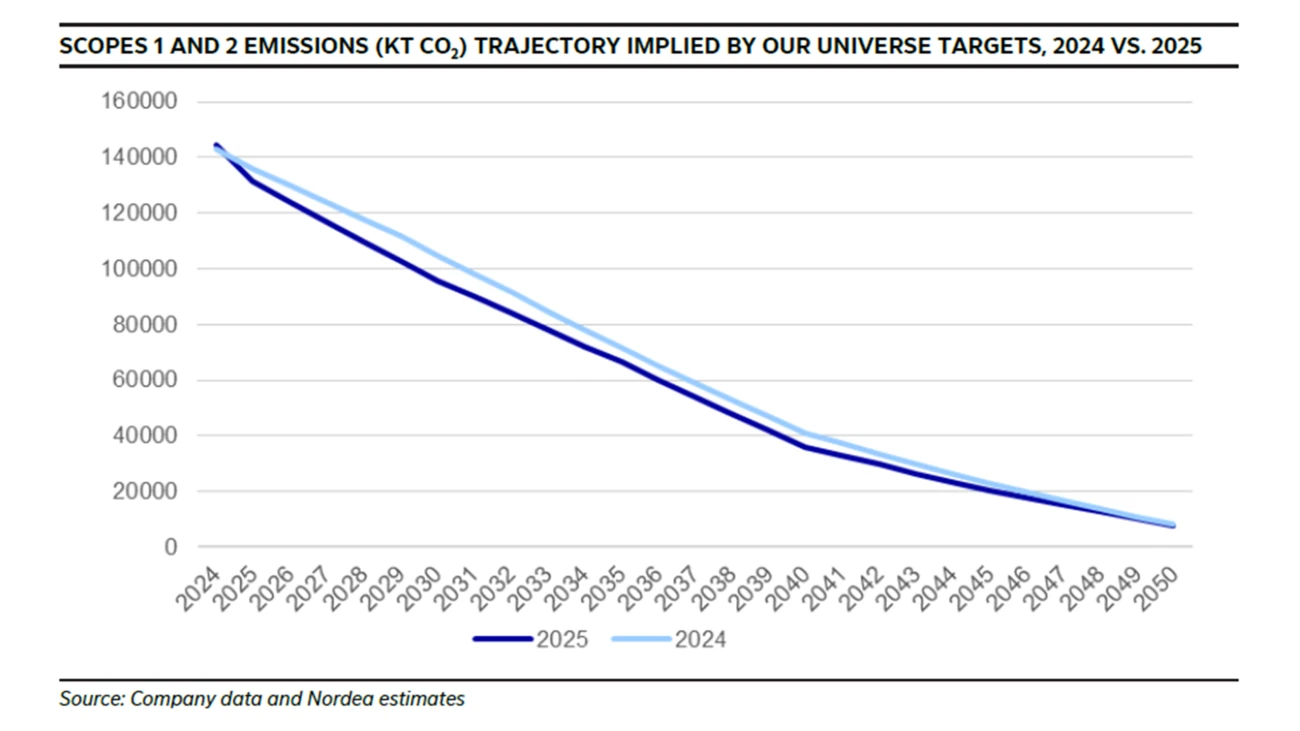

If achieved, the companies’ targets point to an implied temperature rise of 1.5-1.7°C, assuming the global decarbonisation trajectory mirrored that of our Nordic universe. Factoring in Scope 3 emissions complicates the picture: the implied temperature climbs to 2°C, and the likelihood of delivery falls substantially. But we see most companies actively trying to address this gap.

If achieved, the companies’ targets point to an implied temperature rise of 1.5-1.7°C.

This trajectory hinges entirely on companies’ ability to deliver on their targets, and therefore comes with a great deal of uncertainty. But it is substantially better than the global trajectory of 2.7°C.

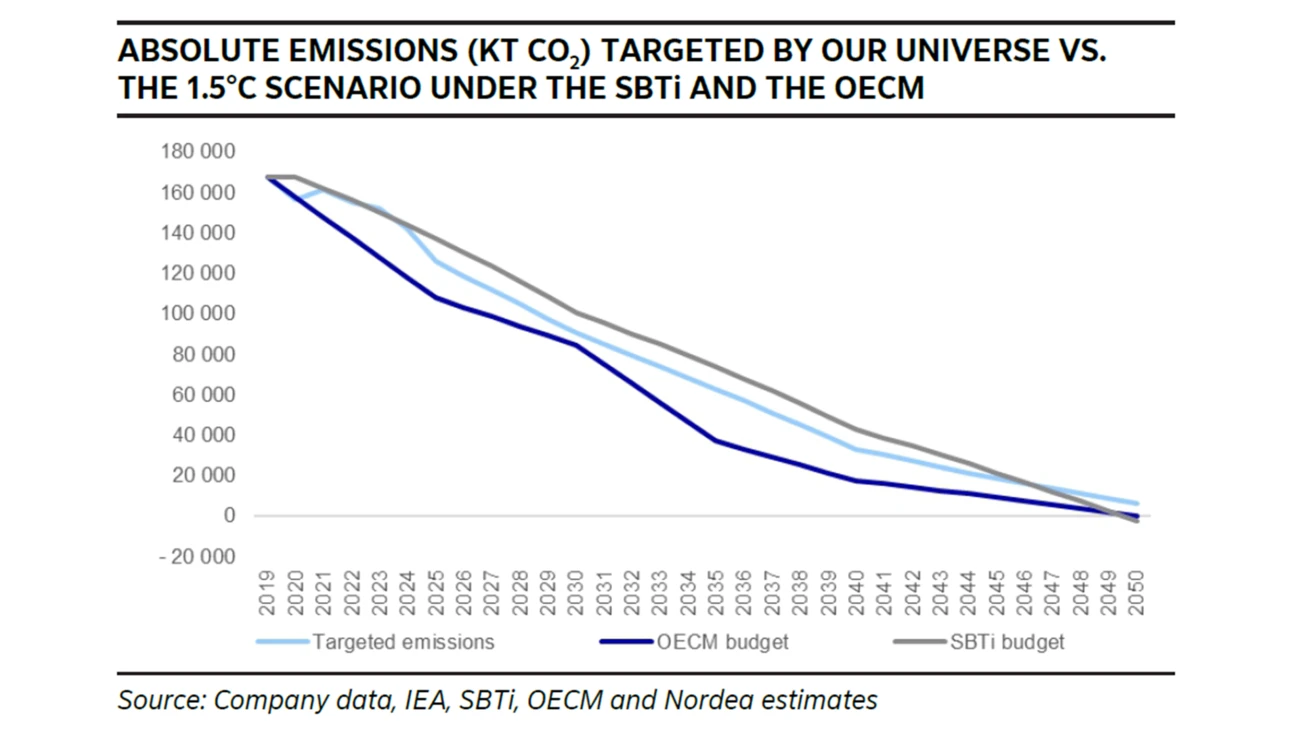

We also assessed companies’ delivery against their targets and find that roughly half of the companies in our coverage universe are on track to achieve their Scope 1 and 2 targets. Weighted for emissions, we view only around 15% of our universe as unlikely to be on track. That means that, so far, large emitters appear to be broadly on track with their Scopes 1 and 2 commitments.

Source: Company data and Nordea estimates

Source: Company data and Nordea estimates

Source: Company data and Nordea estimates

Adding Scope 3 complicates the picture, as we assess that around 50% of our companies are unlikely to be on track. More efforts are clearly required on this front. However, most companies are taking steps, and the decline is likely to accelerate in the coming years, thanks to the combined effect of increased electrification in supply chains and renewables penetration in power grids.

In an era of faltering consensus around climate action, delivery on Scope 3 reductions is a powerful way for Nordic companies to drive decarbonisation globally.

Register below for the latest insights from Nordea’s Sustainable Finance Advisory team direct to your mailbox.

Read more

Sustainable banking

Morningstar Sustainalytics has recently published a new report identifying companies that are taking steps to reduce emissions, set actionable targets and implement good governance practices. Nordea is highlighted for its significant progress in reducing emissions and its comprehensive climate targets.

Read more

Sector insights

As Europe shifts towards strategic autonomy in critical resources, Nordic companies are uniquely positioned to lead. Learn how Nordic companies stand to gain in this new era of managed openness and resource security.

Read more

Open banking

The financial industry is right now in the middle of a paradigm shift as real-time payments become the norm rather than the exception. At the heart of this transformation are banking APIs (application programming interfaces) that enable instant, secure and programmable money movement.

Read more