Key takeaways:

- Electric vehicles offer significant cost advantages in the Nordics.

- The commercial vehicle transition lags passenger cars across the region.

- EU regulation will help accelerate the shift.

Denne siden findes ikke på norsk

Bli værende på denne siden | Fortsett til en lignende side på norsk6 min to read

The transition of Nordic commercial transport towards lower emissions is clearly underway, but it still lags passenger transport. Tightening regulation, low Nordic electricity prices and improving technology are pushing the sector toward electrification, despite significant investment requirements. Electric passenger cars, vans, trucks and buses can deliver lower operating costs and significantly lower emissions, but large-scale adoption still depends on charging infrastructure, grid capacity and further technological development. Across the Nordics, the transition is progressing – though at different speeds.

Road transport is a major contributor to both global oil demand and greenhouse gas emissions, accounting for around 16% of greenhouse gas emissions, with commercial vehicles—trucks, vans and buses—responsible for a significant share. Recent geopolitical tensions in the Strait of Hormuz have pushed oil and gas prices higher, increasing transport and logistics costs across value chains. While the Nordic countries have made strong progress in advancing greener transport solutions, these cost pressures remain evident.

The table below illustrates the cost of driving 100 kilometres using different fuel types for a light commercial vehicle, such as a passenger car.

Nordic fuel price comparison for light vehicles: Prices per 100 kilometres (May 2026)

| Country | Electricity (20kwh/100km) | Petrol 95 E10 (6,3l/100km) | Diesel (6,4l/100km) | CNG / Gas (4kg/100km) | LPG (8l/100km) | Hydrogen |

|---|---|---|---|---|---|---|

| Denmark | 6,60 € | 14,43 € | 14,05 € | 9,80 € | 18,08 € | N/A |

| Finland | 4,40 € | 13,04 € | 14,98 € | 9,00 € | 16,40 € | N/A |

| Norway | 3,80 € | 12,60 € | 11,84 € | 11,80 € | 10,96 € | N/A |

| Sweden | 5,40 € | 10,57 € | 12,07 € | 14,05 € | 12,24 € | 16,80 € |

Source: Eurostat, Konsumentverket, SSB, Tilastokeskus, Bilveden

For larger vehicles (trucks or buses), the average consumption, and therefore cost exposure, is significantly higher than for light vehicles. The average consumption of heavy-duty vehicles (HDVs), referring to a combination vehicle weighing around 60 tonnes, can range between 30 and 75 litres per 100 km. In comparison, an electric vehicle of the same weight consumes roughly 180 kWh per 100 km under summer conditions.

While electric trucks remain more expensive to purchase than diesel trucks, their total cost of ownership is expected to converge over time, particularly in markets with relatively low electricity prices. This cost dynamic is especially relevant in the Nordic region. Based on official electricity and fuel price data, the cost of driving 100 km on electricity remains significantly lower than diesel across the Nordics for all vehicle types. Indicative estimates point to electricity costs of around EUR 3.8–6.6 per 100 km for smaller vehicles, compared with roughly EUR 11.8–15.0 for diesel, depending on the country. For heavy-duty operators, where both consumption and annual mileage are high, this operating cost gap can become strategically important.

In passenger cars, the transition is already well advanced: Norway has effectively reached a fully electric new-car market, while Denmark, Sweden and Finland have all achieved high shares of rechargeable vehicles in new registrations in recent years (read our previous article on the electrification of road transportation). In 2025, rechargeable passenger cars accounted for around 66% of new registrations in Denmark, 60% in Sweden, 57% in Finland and over 90% in Norway.

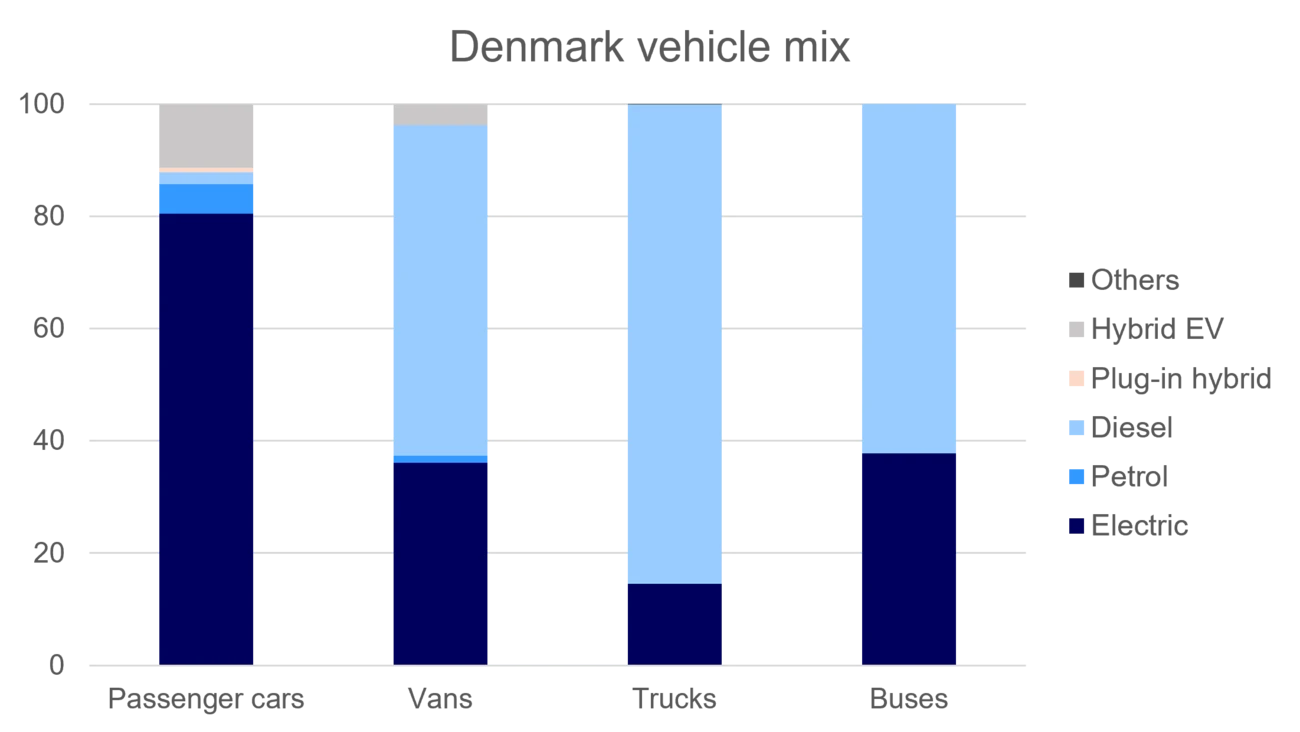

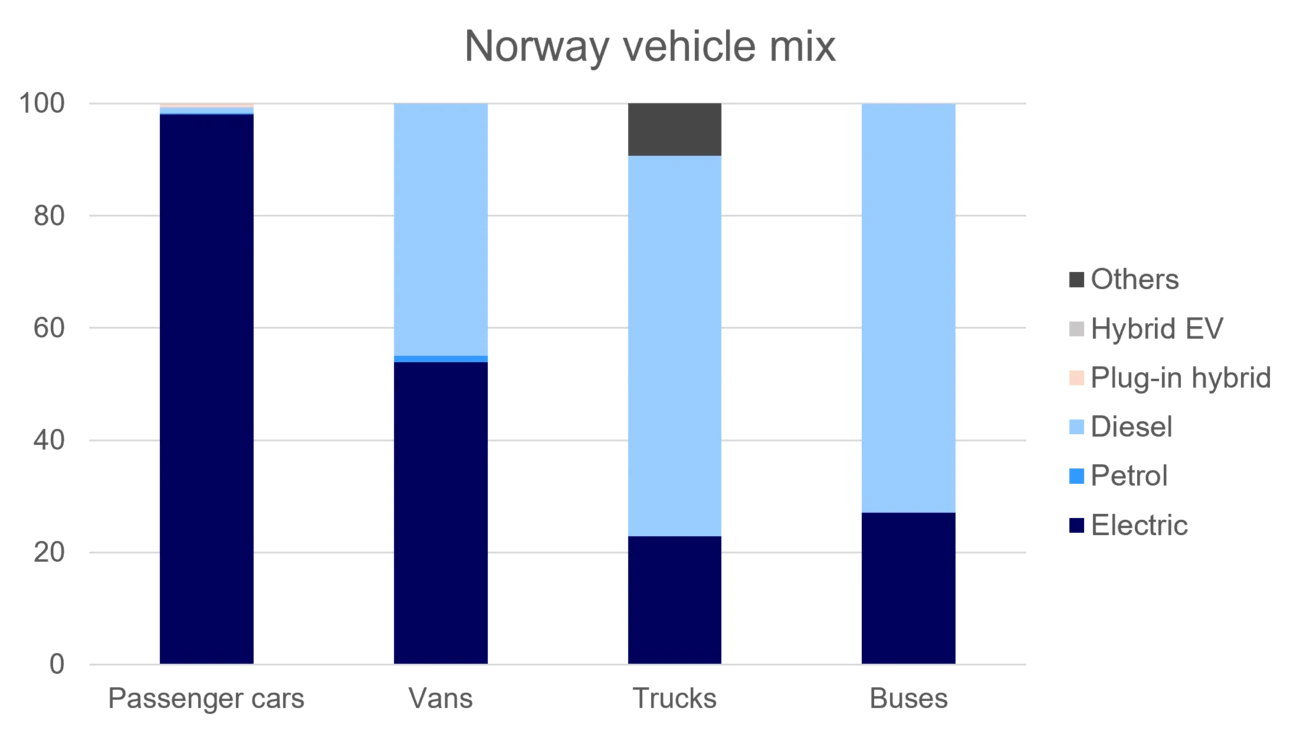

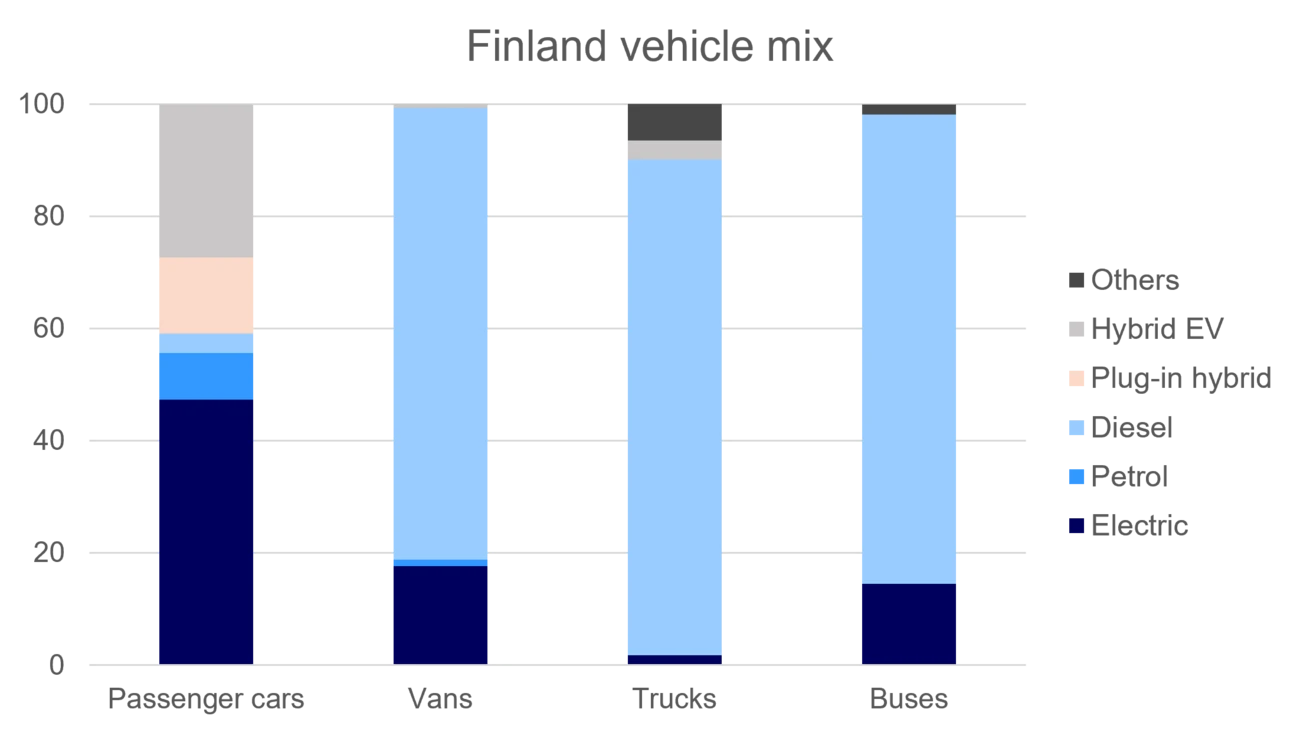

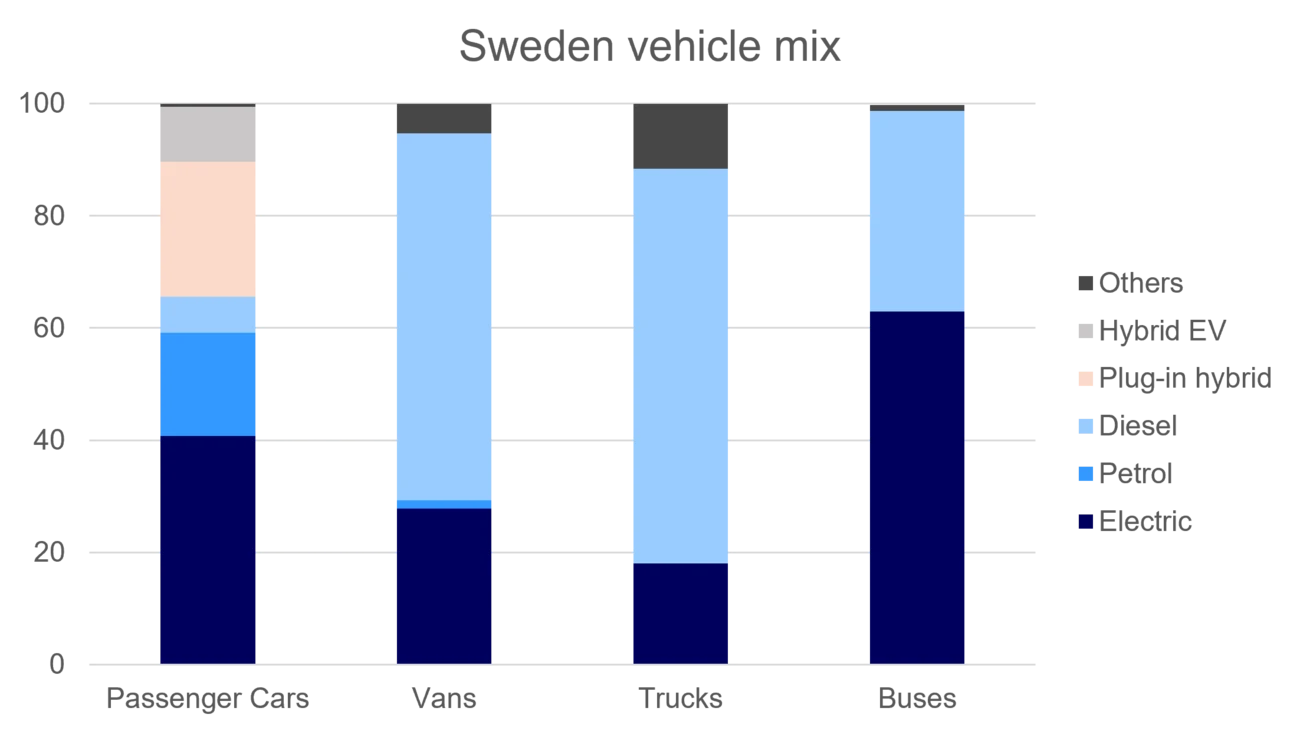

This trend has continued. Norway remains clearly ahead, with more than 98% of new car registrations in 2026 being electric. Denmark has also accelerated significantly, with electric vehicles now making up over 80% of new car registrations. Finland and Sweden continue to record an over 40% share of electric vehicles along with a substantial share of hybrid electric and plug-in hybrid electric vehicle (PHEV) registrations.

Source: ACEA, national statistics

While the Nordic countries are widely seen as leaders in transport electrification in Europe, the transition in commercial vehicles remains at a relatively early stage. Progress is visible across the region, particularly in buses, selected commercial vehicle segments and charging infrastructure, but it remains slow relative to the scale of decarbonisation required. Vans continue to lag behind, reflecting a broader European pattern where available technologies have yet to translate into sufficiently strong demand. In heavy-duty transport more broadly, high purchase costs, limited charging infrastructure, operational constraints and uneven economic incentives continue to slow adoption.

Against this backdrop, progress varies across the Nordic markets.

Norway remains the clear frontrunner, leading the region in commercial vehicle electrification. In early 2026 (January to April), around 41% of new light and heavy commercial vehicle registrations were electric.

Sweden stands out in electric bus registrations, as well as in heavy-duty charging infrastructure and industrial capability. As of November 2025, the country had 129 HDV charging locations, with 97 already meeting the 350 kW Alternative Fuels Infrastructure Regulation (AFIR) threshold, making Sweden the Nordic leader in heavy-duty charging. It is also home to major original equipment manufacturers such as Volvo Trucks and Scania, which gives it a strategic position in zero-emission heavy transport technology.

Denmark is at an earlier stage in the heavy-duty transition, but progress is visible. Denmark offers aggressive incentives to encourage companies to adopt electric vehicles and due to that zero-emission commercial vehicle sales are increasing (up 28.9% year-on-year), infrastructure is expanding, and the country’s compact geography supports electrification economics more than in larger or colder markets.

Finland remains the most challenging market for commercial vehicle electrification in the Nordics. While passenger EV adoption has advanced rapidly, the commercial segment continues to lag. Structural barriers are more pronounced, including long distances, harsh winters, a still-limited HDV charging network and weaker near-term economics for freight electrification. As of December 2025, Finland had only 15 public HDV charging locations and 35 chargers—the lowest figure among the four Nordic countries. At the same time, electric vehicles accounted for only around 1.8% of Finland’s total truck fleet in 2025, according to Autoalan Tiedotuskeskus.

While the Nordic countries are widely seen as leaders in transport electrification in Europe, the transition in commercial vehicles remains at a relatively early stage.

The long-term direction of the road transport sector is increasingly being shaped by a combination of regulatory tightening and voluntary ambition. This marks a structural shift: regulation is now directly influencing investment decisions and accelerating the move away from conventional powertrains.

The revised EU regulation on CO2 standards for heavy-duty vehicles significantly tightened the sector’s decarbonisation pathway. The framework requires a 15% CO2 reduction by 2025, 45% by 2030, 65% by 2035 and 90% by 2040 for covered heavy-duty vehicle categories (EU). In practice, these targets will make it increasingly difficult for manufacturers – and, over time, operators – to rely on diesel-based transportation alone.

At the same time, the Alternative Fuels Infrastructure Regulation (AFIR) is establishing the infrastructure backbone for this transition. By setting minimum requirements for charging and refuelling capacity along key freight corridors, AFIR shifts infrastructure from a voluntary, market-driven rollout to a compliance-driven necessity.

Looking ahead, broader climate policy will reinforce this direction. The extension of carbon pricing and fuel-related climate regulation will increase the cost of fossil-based transport over time, improving the relative competitiveness of low-emission alternatives. For companies and investors, the question is no longer whether Nordic heavy transport will decarbonise, but how quickly different business models can adapt.

Register below for the latest insights from Nordea’s Sustainable Finance Advisory team direct to your mailbox.

Read more

Sustainability

The deadline for national transposition of the EU’s Energy Performance of Buildings Directive (EPBD) has passed, and countries are now legally responsible for the regulation’s renovation targets. We have reviewed trends in France, the most notable EPBD early-adopter, to get clues about potential future impact.

Read more

Insights

Nordea recently supported OX2 in securing project financing for two co-located battery energy storage systems with a combined capacity of 235 MW/470 MWh, integrated with the company's new onshore wind portfolio in Finland.

Read more

Our people

Finnish corporates are shifting gears: from building solid foundations and profitability to pursuing growth. Antti Saha, Head of Large Corporates & Institutions in Finland, explains what’s driving the shift, and why he compares his role to conducting a jazz band.

Read more